Row over hindutva defused as ruling hegemony is unted rock solid to enhance ethnic cleansing!India may target $7.4 billion from stake sales in budget.Petrol prices may be hiked by Re 1/L, diesel by 50 paise/L by Saturday.

Indian Holocaust My Father`s Life and Time, Chapter: Nine Hundred Sixty

Palash Biswas

Mobile: 919903717833

Skype ID: palash.biswas4

Email: palashbiswaskl@gmail.com

Petrol prices may be hiked by Re 1/L, diesel by 50 paise/L by Saturday!Open market economy has overwhelmed Indian culture based on hindutav as an industry body has valued the Valentine's Day (V-Day) market in India at USD 27 million (Rs.15 billion) based on a survey involving 800 executives in major metros and 1,000 students from 150 educational institutions.

Row over Hindutva is blown over and it is gone with the wind. People who live in glass houses do not dare to throw stones on other`s places! It is the most famous dialogue delivered by Rajkumar in a sixties` bollywood film, SHEESHE KE GHAR MEIN JO LOG RAHTE HAIN...Just remember. The UPA Government need excellent floor adjustment in the budget session of parliament to accomplish the agenda of second generation of reforms. The minority government may not afford non cooperation from Sangh Pariwar. Hence,Home Minister Sushilkumar Shinde is all set to defuse the row over his controversial Hindu terror remarks by making a statement in Parliament that he had no intention to hurt anybody.Shinde, who is also Leader of the Lok Sabha, has already stated that he and the Congress believe terrorism has no colour. Congress spokesperson P C Chacko today side-stepped questions on whether Shinde will tender an apology in Parliament to facilitate smooth functioning of the House.n a bid to resolve the impending deadlock, Shinde had reached out to Leader of Opposition in Lok Sabha Sushma Swaraj and her Rajya Sabha counterpart Arun Jaitley.

The Home Minister had reportedly even sent a draft of the statement he intends to make in the House on the issue but it has not satisfied the BJP. The Opposition party is under pressure from Sangh fountainhead RSS to pursue the matter strongly both inside and outside Parliament and force Shinde to apologise. The party had earlier even demanded that if Shinde does not apologise then he should be sacked.

Row over hindutva defuged as ruling hegemony is unted rock solid to enhance ethnic cleansing!India may target $7.4 billion from stake sales in budget.The government is likely to target 400 billion rupees in proceeds from stake sales in state-run companies in the next fiscal year, a finance ministry official with direct knowledge of budget talks told Reuters on Wednesday.The official also said the government is likely to allocate 200 billion rupees for capital infusions into state-run banks in the next financial year, up from 150 billion rupees set aside for bank recapitalisation in the current year.Meanwhile, contrary to the much hyped growth story,India posted its second highest ever monthly trade deficit of $20 billion in January as imports surged to record highs, piling pressure on a widening current account deficit and limiting scope for the RBI to cut interest rates.On the other hand,Italy's Economy Ministry on Tuesday said that it was working to provide management continuity and protect shareholder interest at state-owned defence group Finmeccanica (SIFI.MI), according to a statement.However,Moody's Investor Services on Tuesday said downside risks for the global economy had receded in the past three months, though a number of dangers still remained.The World Bank's new chief economist on Tuesday urged Group of 20 finance leaders to better coordinate economic policies in order to prevent a possible global currency war.India's annual consumer price inflation accelerated to 10.79 percent in January from the previous month, government data showed on Tuesday.

"The ministry is working to ensure that the company rapidly adopts a governance system that is able to guarantee the needed management continuity, the protection of shareholders' interests - and therefore of the taxpayer - and the maximum correctness and transparency in decision making," the statement said.Finmeccanica Chief Executive and Chairman Giuseppe Orsi was arrested Tuesday over bribes allegedly paid to secure the sale of 12 helicopters to India when he was head of the group's AgustaWestland unit, a judicial source with direct knowledge of the situation told Reuters. India has suspended payments to Italian defence group Finmeccanica SpA (SIFI.MI) for a $750 million helicopter deal and won't take delivery of more aircraft until the completion of a Central Bureau of Investigation (CBI) probe into bribery allegations, a defence ministry source told Reuters.

Petrol price may be hiked by about Re 1 a litre and diesel by 50 paise a litre by this weekend as oil firms begin to exercise the recently accorded freedom to adjust rates in step with cost.

State-owned oil firms are losing Rs 1.32 a litre on petrol as international oil rates have firmed up during the last two weeks. They intend to pass on most of the loss to consumer at the next review due on February 15.

Also, diesel prices may be increased by 40-50 paise a litre in line with the freedom given by the government last month to raise rates of India's most consumed fuel in small dozes every month till such time that the Rs 9.22 a litre loss is completely wiped out.

"Gasoline (petrol) prices in international market are rising. The trend shows that we will have under-recoveries (losses) on petrol," said R S Butola, Chairman of Indian Oil Corp, the nation's largest fuel retailer.

"We will review the prices at the fortnightly review (due on February 15)," he said. "We won't say there is no possibility (of a price increase) but I cannot say what we will decide in that review."

Sources said FOB price of gasoline have risen from USD 123 per barrel, against which the retail petrol rates are benchmarked, to USD 131.

Petrol price was last revised on January 18 when the price was cut by 30 paise to Rs 67.26 a litre in Delhi.

The reduction in rates coincided with government decision to give oil firms freedom to raise diesel prices in small monthly dozes to eliminate all of the losses on the fuel. Oil firms hiked diesel price on that day by 50 paise to Rs 47.65 a litre in Delhi.

"We will review the prices when they are next due. I cannot say if we will change them or not," Butola said.

Sources said the oil firms may decide not to pass on the entire loss on petrol in one go and the likely increase could range anywhere between 50 paise to Re 1. Diesel rates in all probability are likely to be hiked by 40 to 50 paise a litre.

Butola said oil firms are currently losing Rs 9.22 a litre on diesel, Rs 31.60 a litre on kerosene and Rs 481.03 per 14.2-kg LPG cylinder.

The revenue target from a partial privatisation of state-run companies is higher than the 300 billion rupees New Delhi is aiming for in the current fiscal year that ends in March.

With less than two months to go before the year closes, the government has managed to raise 70 percent of the targeted amount, and officials in the government concede that the final figures for this year could fall shy of the target.

The struggle to meet the current year's target had made many investment bankers believe that the government would likely budget at least 300 billion rupees for next fiscal year as well.

But a resource crunch has forced New Delhi to aim higher, said the official, who declined to be identified because he was not authorised to speak about the budget, to be released on February 28.

"The aim is to maximise your revenue options. Low growth has constrained our resources," the official said. The government is still to finalise the target, he said.

India needs to augment its revenues to help lower the fiscal deficit to its targeted 4.8 percent of gross domestic product in the financial year that begins on April 1. A swollen deficit has put the country's investment grade credit rating in peril.

The planned capital injection into state banks, while higher than in the current year, still falls short of their capital requirements. The central bank said in September that the government needed to infuse 900 billion rupees into state-run banks to meet upcoming Basel III requirements.

India's state-run banks face rising bad assets as companies struggle to pay off loans in a sluggish economy.

The official said the government would likely infuse capital in 12 banks, including State Bank of India, the country's largest lender.

The government this month approved a plan to inject around 30 billion rupees in State Bank of India through preferential allotment of shares.

Struggling to turn around an economy that is slowing to its lowest growth rate in a decade, the Reserve Bank of India cut interest rates by 0.25 percentage points last month, but warned that future rate cuts would depend upon declines in both the current account deficit and inflation.

But there was little sign of any respite on the external front for Asia's third largest economy in December as a surge in imports dwarfed a slight improvement in exports.

Exports rose an annual 0.8 percent to $25.59 billion in January, the first time they have risen since the start of the fiscal year in April last year, on the back of better sales of engineering goods, drugs and gems.

But imports rose 6 percent to $45.58 billion, according to a senior trade ministry official, their highest ever monthly total. Imports of oil, the single biggest item, rose 6.9 percent from a year ago to $15.9 billion.

"The oil import bill is definitely a challenge, but for a growing economy, energy needs have to be met," Commerce and Industry Minister Anand Sharma told an industry conference in Mumbai.

The January trade deficit was the second worst on record. The worst figure was $20.9 billion posted in October.

Current account data for the October-December quarter will be released at the end of next month, but the deficit touched a record high in September at 5.4 percent of GDP due to slowing exports and heavy oil and gold imports.

NEW PRESSURE ON THE RUPEE

The Reserve Bank of India is worried that India's ability to fund its rising current account deficit is becoming increasingly stretched, and could lead to fresh pressure on the rupee.

"The high current account deficit is unsustainable as it can't be funded for a long time with capital flows and it will get adjusted through the exchange rate," said A. Prasanna, economist, ICICI Securities Primary Dealership. "The exchange rate will depreciate when the correction happens."

The rupee struck its weakest in over a month in early January at 55.38 to the dollar, but has since recovered on capital inflows. The rupee strengthened marginally to 53.84 to the dollar after the data, as some traders had priced in an even wider trade deficit.

Exports between April and January fell 4.9 percent to $239.7 billion, pushing the cumulative trade deficit for the first 10 months of the fiscal year to $167.2 billion, up 8 percent on the same period a year earlier. Sluggish demand from the United States and Europe has crimped India's exports.

Samiran Chakraborty, an economist at Standard Chartered Bank in Mumbai, said the trade deficit's deterioration in January was a concern, as it would typically be expected to improve during the January-March quarter, but a surge in gold imports in anticipation of a recent import duty may have been a factor.

The government did not detail imports of gold, usually the second-biggest item.

On Monday, Reserve Bank of India Governor Duvvuri Subbarao reiterated concern over financing the current account deficit with volatile capital flows. Portfolio inflows into India have been robust, with $8.34 billion so far this year after inflows of $31.41 billion in the whole of 2012.

Subbarao projected a record high current account deficit for the 2012/13 fiscal year, ending in March. Many analysts expect the deficit to rise from 4.2 percent of gross domestic product in 2011/12 to a record 4.5-5.0 percent of GDP for 2012/13.

Sebi freezes Sahara accounts, attaches property

Coming down heavily on Saharas in investor refund case involving over Rs 24,000 crore, regulator Sebi on Wednesday ordered freezing of bank accounts and attachment of all investments and properties of two Sahara firms and their top executives, including group chief Subrata Roy.

The assets being attached include those related to the group's Aambey Valley resort town near Pune, other real estate assets in Delhi, Mumbai and at other places across the country, shares, mutual funds and various other investments.

Sebi's action comes within days of the Supreme Court saying that the market regulator was free to freeze accounts and attach properties if Sahara group firms were not depositing the money with it for refund to investors.

Passing two separate orders, together running into 160 pages, against Sahara Housing Investment Corporation Ltd (SHICL) and Sahara India Real Estate Corporation Ltd (SIRECL), Sebi said that the two companies had raised Rs 6,380 crore and Rs 19,400 crore respectively from bondholders and "various illegalities" were committed in raising of these funds.

With regard to Subrata Roy and three other directors, namely Vandana Bhargava, Ravi Shanker Dubey and Ashok Roy Choudhary, Sebi ordered freezing of all bank and demat accounts of these four persons, as also attachment of all movable and immovable properties in their name with immediate effect.

Sahara group was yet to comment on the orders despite repeated attempts.

The Supreme Court on August 31, 2012, had asked Sahara group firms to refund the money with 15 per cent interest and had asked Sebi to facilitate the refund.

However, the group in December 2012, was allowed to pay the money in three instalments, including an immediate payment of Rs 5,120 crore, followed by an instalment of Rs 10,000 crore in the first week of January and remainder by the first week of February 2013.

In its orders passed today, Sebi said that neither of the two instalments was paid and therefore it is constrained to take necessary action as per the Supreme Court orders.

With regard to the payment of Rs 5,120 crore also, Saharas have claimed that only Rs 2620 crore remained to be refunded to investors and it has already paid Rs 19,400 crore to the bondholders, Sebi said, adding it has been forced to take further actions.

The properties being attached by Sebi include the land owned by Sahara group firm Aamby Valley Ltd, which has set up a resort village near Pune, development rights of land at prime locations in Delhi, Gurgaon, Mumbai and various other places across the country.

Besides, Sebi has also ordered attachment of equity shares held in Aamby Valley Ltd, units of mutual funds, bank and demat accounts and investments in all the branches of all banks. Sebi has asked all the banks to transfer the amounts lying in those accounts to its Sebi-Sahara Refund Account.

Sebi also directed Subrata Roy and three other directors to furnish details of all movable and immovable properties in their name within 21 days, pending which they can not alienate, dispose or encumber any of their assets.

The regulator said it is seeking attachment of all other movable and immovable properties owned and/or held by the two companies SIRECL with immediate effect and asked them not to "alienate, dispose or in any manner encumber the same".

Sebi also directed the two firms to furnish details of any other investments within 21 days and restrained them with immediate effect from operating their bank and demat accounts and from withdrawing of any investments.

The two companies have also been asked to deposit cash, bank balances and fixed deposits in their names to Sebi and have also been barred from transferring any shares held by them.

Sebi said it has informed RBI and Enforcement Directorate as well regarding its actions against Sahara group firms. The assets being attached include investments of SIRECL and SHICL in group companies, special purpose vehicles and partnership firms and the necessary orders for sale of all attached properties would be passed in due course after getting their full particulars, Sebi said.

Many states differ on provisions of Food Bill

In a setback to Food Security Bill, considered as the world's biggest welfare programme, many of the states on Wednesday differed on the quantity of subsidised grain to be supplied and the number of beneficiaries to be covered under the scheme.

The consultation meeting of state food ministers was organised here to evolve a consensus on recommendations of the Parliamentary panel that suggested drastic changes in the proposed Food Bill, which aims to give legal right over subsidised foodgrains to two-thirds of the population.

Tamil Nadu sought complete exemption from the implementation of the bill saying it lacked clarity, while states like Bihar, Orissa, Kerala, Punjab and Gujarat suggested the Centre first modernise Public Distribution System (PDS) before rushing to implement it.

Asked if lack of consensus on the Bill will delay Food bill, Union Food Minister K V Thomas said separately, "Except Tamil Nadu, all states have welcomed the bill.

Some have expressed reservation on certain provisions. ...We cannot satisfy all states. We intend to present the revised bill in the forthcoming session of Parliament."

Tamil Nadu, West Bengal and Chhattisgarh pitched for universal public distribution system (PDS), whereas Orissa, Kerala and Bihar, among others, said the foodgrains quantity of 5 kg per person per month suggested by the Parliamentary panel was not sufficient and sought higher allocation.

Tamil Nadu Food Minister R Kamaraj said: "I insist that the government should exempt Tamil Nadu from implementation of the proposed Food Bill and allow the state to implement the existing universal PDS as it is more effective".

"The bill is replete with confusion and inaccuracy and there is no clarity on identification of beneficiaries".

The consultation meeting, attended by 19 states and UTs, saw many states suggesting identification of beneficiaries be left to them. They said it would be difficult to bear additional expenses of implementing the bill due to financial stress.

Many states also opposed cash transfer of subsidy saying it cannot be a substitute for foodgrains. Barring one state, most of them favoured providing nutritional security to pregnant women and children under the bill.

On beneficiaries, Bihar Food Minister Shyam Razak said, "The socio economic caste census (SECC) is yet to be completed. Meanwhile, BPL Commission should be set up to identify beneficiaries consulting respective states."

He also said the Centre should not be in a hurry to implement the bill without modernising PDS.

At the same time, Punjab Food Minister Adaish Pratap Singh emphasised exclusion criteria should be decided in consultation with state governments, while Orissa Food Minister Pratab Keshri Deb sought inclusion of tribal population without capping coverage of population.

Meanwhile, Gujarat Food Minister Bhupendrasinh Manubha said: "The Bill suffers from enormous uncertainties in terms of likely number of beneficiaries, requirement and availability of foodgrains on a sustainable basis."

At the beginning of consultation meeting, Union Food Minister KV Thomas had said that there are divergent views on certain provisions of the bill. The challenge is "to arrive at a workable, practical and equitable approach, keeping the larger objective of the bill in mind," he added.

Stating this is the last opportunity for consultation before finalising the Bill, Thomas said,"We need to finalise our views on these recommendations early, give a final shape to the Bill and present it back to Parliament for consideration and passage in the ensuing Budget session."

The views of the state governments are "extremely important" as "still there are certain aspects which need to be discussed before taking a final view."

According to the recommendation of a Parliamentary panel, all the beneficiaries, without categorising them as priority and general households, be given 5 kg of wheat and rice per month at a uniform rate of Rs 2 and Rs 3 per kg, respectively, under the proposed Food bill.

Whereas the Centre had proposed 7 kg foodgrains per person to priority households at cheaper rate and 3kg to general household at half of the support price.

At present, below poverty line (BPL) families effectively get 7 kg of wheat and rice at Rs 4.15 and Rs 5.65 per kg respectively per month.

If the Parliamentary panel's recommendations are accepted, it will benefit the general population in both price and quantity, while BPL members could get lesser quota than what was proposed in the original Bill.

Prez Pranab rejects mercy pleas of Veerappan aides

Days after rejecting the mercy petitions of 26/11 attacker Ajmal Kasab and Parliament attack case convict Afzal Guru, President Pranab Mukherjee has dismissed four more mercy pleas, reports said on Wednesday.

As per reports, the President rejected the mercy petitions moved by four associates of late forest brigand Veerappan.

The four Veerappan aides were sentenced to death in a landmine blast case in Karnataka.

An advocate S Balamurugan, appearing for the accused, said, "We have received information from reliable sources that the message has been sent to Belgaum jail authorities and apparently it has also been conveyed to the prisoners."

Balalmurugan, who is also the Tamil Nadu PUCL state secretary, gave this information to mediamen.

The dreaded sandalwood bandit Veerappan was killed in an encounter with the Tamil Nadu police of the special task force in October 2004.

The four accused, Gnanprakasham, Simon, Meesekar Madaiah and Bilavendran, were sentenced to death by the Supreme Court in January 2004 in connection with the killing of 21 policemen in a landmine blast at Palar in Karnataka near the inter-state border in 1993. T

They were sentenced to undergo life imprisonment by the Mysore court. But the government moved the Supreme Court, which awarded them the death sentence. Their mercy pleas have been pending since 2004.

Market Action |

- INDIA

- SECTORS

- GAINERS/LOSERS

- WORLD

19608.08 47.04 (0.24%)

NIFTY

5932.95 10.45 (0.18%)

Nifty closes off day high; United Breweries, MCX big losers

7:02 PM Buy ONGC; target of Rs 357: Angel Broking -See more in Stocks Views | Check ONGC |

FIPB clears 4 single-brand retail FDI proposals

The Finance Ministry today cleared four foreign direct investment (FDI) proposals in single brand retailing, including that of Decathlon and Fossil Inc, worth about Rs 750 crore, sources said.

* * |

The Finance Ministry today cleared four foreign direct investment (FDI) proposals in single brand retailing, including that of Decathlon and Fossil Inc, worth about Rs 750 crore, sources said. Foreign Investment Promotion Board (FIPB), headed by Economic Affairs Secretary Arvind Mayaram, in its meeting has also cleared the proposals of French fashion brand Promod, crockery maker Le Creuset and sports giant Decathlon, they said.

India is witnessing an increased interest in the retailing segment, ever since the government allowed 100 per cent FDI in single brand retail in January 2012. The proposal of Le Creuset, Fossil Inc, and Decathlon were for 100 per cent FDI, while Promod sought entering the segment through a joint venture.

Decathlon alone would bring in foreign equity worth Rs 700 crore, while Promod would bring about Rs 30 crore and the American high-end accessories firm Fossil Inc plans over Rs 22 crore investment. Crockery maker Le Creuset, which already operates a cash-and-carry business in India, may not bring in fresh investment but rather get funding from its existing wholesale operations, they added.

In the recent past, the FIPB has cleared several major single brand retail proposals including that of Swedish furniture-maker IKEA, British footwear retailer Pavers England, American luxury clothing retailer Brooks Brothers and Italian jewellery maker Damiani.

http://www.moneycontrol.com/news/economy/fipb-clears-4-single-brand-retail-fdi-proposals_823762.html

India-US keen on co-producing and exporting arms

If everything goes well, India-US strategic defence co-operation will go beyond joint military exercises, and would enter into the realm of co-producing, and jointly exporting the arms to other countries.

WASHINGTON: India not only wants to co-develop and co-produce arms with the US, but also wants to jointly export them, a top Pentagon official has said adding that the United States supports such Indian aspirations.

"The Indians don't want to just buy weapons systems from us, they want to co-develop and co-produce systems of mutual value...that we can jointly export," US Deputy Defence Secretary Ashton B Carter has said following his recent meeting with National Security Advisor Shivshankar Menon, in Germany on the sidelines of the 49th Munich Security Conference.

"The two had a positive discussion concerning issues of mutual interest," a Pentagon spokeswoman told PTI after the Carter-Menon meeting.

"We support that aspiration in India. That's the way we want to do things, too," Carter told American Forces Press Service aboard his aircraft during his return flight following his six-day international trip that took him to Paris, Munich, Turkey and Jordan.

Carter had last visited India in July last year, soon after the visit of US Defence Secretary Leon Panetta.

It is during this trip that Panetta had announced that Carter had been entrusted with the task of working with Indian officials to reduce bureaucratic hurdles to increase defence trade between India and the United States.

In his meeting with Menon, Carter discussed progress that has been made on these efforts.

During his India trip, Carter had also visited the facilities in Hyderabad where India's Tata Advanced SystemsLimited and US-based Lockheed Martin produce parts for the C-130J, the "Super Hercules" four-engine military transport aircraft that Lockheed produces.

"The Indians are buying the C-130J, but they're also building the C-130J...and that's a perfect example of the kind of project we want to do with India," Carter said.

Retail inflation at 10.79%: Why food prices are not falling

Analysts do not see prices of food items coming down anytime soon and have blamed supply side constraints for a consistently high number.

NEW DELHI: Rising for the fourth consecutive month,retail inflation remained in double digits at 10.79 per cent in January, driven by higher prices of vegetables, edible oil, cereals and protein-based items. The country's retail inflation is the highest among theBRICS group of emerging economies - Brazil, Russia, China, and South Africa.

Analysts do not see prices of food items coming down anytime soon and have blamed supply side constraints for a consistently high number. Nitesh Ranjan, Economist, Union Bank of India expressed disappointment at the high CPI number.

"We have seen that food inflation has remained high even in the WPI. I do not expect pressures from the food side to ease anytime soon, so expect the CPI to remain high for some more time," Ranjan said.

Dr Brinda Jagirdar, General Manager & Head Economic Research expects food inflation to remain sticky and blames supply side contraints for it being so high. "We expect food price inflation to remain sticky for a while mainly because there has not been a great pickup from the supply side. The per capital availability of cereals has been declining," Jagirdar told ET Now.

"India is the largest producer of fruits and vegetables. Yet, we are unable to meet the demand. We are also the largest producer of milk. We need to take measures on the food processing and distribution side. We need to tackle inflation so that consumption demand picks up," Jagirdar opined.

"Softening in inflation is on account of a decline in core inflation and from the manufacturing side. This is because global commodity prices are softening and pricing power has also been declining. Therefore, manufactures are not able to pass on any hike. We expect WPI to decline to around 6.8% to 7%," Jagirdar added.

The vegetables basket in January recorded the highest inflation of 26.11 per cent among all the constituents that make the Consumer Price Index (CPI), according to data released.

Vegetables were followed by the oil and fats segment at 14.98 per cent. Meat, fish and egg became 13.73 per cent more expensive during the month.

While, cereals and pulses became dearer by 14.90 per cent and 12.76 per cent respectively on an annual basis, sugar turned more expensive by 12.95 per cent.

Clothing and footwear witnessed 11 per cent increase in prices during the month.

In urban areas, retail inflation rose to 10.73 per cent in January from 10.42 per cent in the previous month. The CPI for rural population increased to 10.88 per cent during the month from 10.74 per cent in December.

The data for wholesale price index (WPI)-based inflation is expected on Thursday. The WPI figures for December stood at 7.24 per cent, much higher than RBI's comfort level of 5-6 per cent.

The Reserve Bank of India (RBI) in its monetary policy last month had slashed its key interest rates by 0.25 per cent and released Rs 18,000 crore additional liquidity into the system to perk up growth through reduced cost of borrowing.

The RBI has forecast the March end WPI inflation at 6.8 per cent.

Meanwhile, industrial output growth rate contracted by 0.6 per cent in December, 2012, compared to a growth of 2.7 per cent in same month a year ago.

Tue, Feb 12, 2013 at 17:42

Industrial growth for December 2012: CARE Ratings

CARE Ratings has come out with its report on "IIP growth for December 2012". According to the rating agency, the growth of 6.8% in community, social and personal services seems difficult to attain with an expectation of reduced government spending in the coming months.

| * |

CARE Ratings has come out with its report on "IIP growth for December 2012". According to the rating agency, the growth of 6.8% in community, social and personal services seems difficult to attain with an expectation of reduced government spending in the coming months.

The Central Statistics Office (CSO) has released the data for industrial production for the month of December 2012. Continuing with the decline in industrial production, IIP for the month of December 2012 registered a growth of -0.6% compared with 2.7% for the same period last fiscal. The negative growth has been primarily influenced by contraction in mining and manufacturing activities. This is the sixth month in the year where growth has slipped into negative territory.

Cumulative growth in FY13 in Apr- Dec 2012 stands at 0.7% as against a growth of 3.7% in corresponding period of the previous year.

Cumulative Picture: (Apr- Dec FY13 over Apr- Dec FY12)

Mining registered -1.9% growth in April Dec 2012, as against -2.6% during the same period last year

Manufacturing registered near zero growth of 0.7% in April - Dec 2012, when compared with 4.0% in April - Dec 2011.

Relatively high growth rates witnessed in case of radio, TV etc, coke, refined petroleum, textiles and luggage etc.

Growth in electricity has moderated to 4.6% in April Dec 2012, as against 9.6% in same period last year.

Policy Action

Last month, the Reserve Bank of India (RBI) cut policy rates by 25 basis points for the first time in nine months to boost growth as inflation showed signs of moderation. The RBI's monetary policy is primarily influenced by the inflation numbers. The January CPI number came in at 10.79%, indicating high retail inflation. There is an expectation of another 25 bps cut in repo rates, however the RBI's March policy action would be dependent on the FY14 budget which is to be presented on 28th February 2013.

Conclusion

Belying expectations that the factory output cycle had turned; index of industrial production (IIP) for the month of December came in at -0.6%, below CARE's own estimates of 2.17%. The Central Statistics Office (CSO) last week projected economic growth would decelerate to a decade's low at 5% in 2012-13 beating expectations on the downside. Official sources are still hopeful of 5.5% or more during the year, hoping for a turnaround. We however feel that the CSO estimate of 5% seems more likely to be achieved with a downward bias. The growth of 6.8% in community, social and personal services seems difficult to attain with an expectation of reduced government spending in the coming months.

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on moneycontrol.com are their own, and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

http://www.moneycontrol.com/news/care-research/industrial-growth-for-december-2012-care-ratings_822667.html

Companies Bill to come up in Rajya Sabha in Budget session: Sachin Pilot

Companies Bill to come up in Rajya Sabha in Budget session: Sachin Pilot

MUMBAI: Corporate Affairs Minister Sachin Pilot today said the government is confident of getting the newCompanies Bill passed in the Rajya Sabha in the Budget session. "The new Companies Bill will come up in the Rajya Sabha in the Budget session beginning February 21," Pilot said on the sidelines of the Nasscom national summit here.

Noting that since the enactment of the Companies Bill in 1956, the number of registered companies has gone up to 8.5 lakh, Pilot said the new Bill aims to address transformations that have taken place in the last few years such as the emergence of e-commerce companies.

Pointing out that there are e-commerce companies that do business here but may be present outside or have no physical presence here at all, he said, adding the law needs to look at such companies.

Referring to the poor ranking of the country at 132 in the World Bank's list of 185 countries in terms of ease of doing business, Pilot said the ministry has appointed a commission to look into this.

"I don't think we are doing justice by getting India go down in terms of such indices. I hope our ranking will improve in the next few years," he said.

On the mandatory 2 per cent of net profit being spent on corporate social responsibility (CSR) projects, Pilot said the ministry is working on a database that will have details of worthy projects, NGOs and best practises followed in different states, which the companies can refer to while deciding on their strategy.

The ministry is also working on a template to be posted on its website that will require companies to clearly spell out what CSR projects they have undertaken, how much they have spent on this and what tangible benefit has arisen from it, the minister said.

Stating that government is not trying to dictate terms of doing business to private companies, Pilot said the government will adopt a "hands-off approach" and companies would have to self-report and self-comply on their CSR activities.

13 FEB, 2013, 10.57AM IST, GAYATRI NAYAK,ET BUREAU

Only money in circulation can lift the economy

While financial instruments may be good from the nation's point of view, they are not for individual investors.

EDITORS PICK

Finance minister P Chidambaram last week made a passionate case for savings to be routed to financial instruments instead of real assets. In fact, he told a story about a Wharton University professor's investment strategy — after buying a stock, do not look at it at all for years. That is indeed what many successful investors, including Warren Buffett, have been doing for years.

But the reality with individual investors is that everytime the price falls below the purchase price, the heart beat gets faster. Same is the case with mutual fundinvestments — when the net asset value plunges, investors tend to worry. Bonds are literally inaccessible for retail investors, but bank deposits are the nation's favourite because of the security they provide.

But over the years, even bank deposits have become unfavourable, thanks to the partial tax treatment they receive and the artificially-low interest rates that led to a negative return, adjusted for inflation. While financial instruments may be good from the nation's point of view, they are not for individual investors — at least that's what the investor conclusion seems to be.

They believe in what they see — gold and real estate are good for them. If one looks at the two-decade history, both the real assets have not failed investors. Also, individual profiles and behaviour have changed since liberalisation began in 1991. They are saving less, borrowing more and whatever they save goes into that 'barbarous relic' called gold.

There are anomalies that have crept in which work against the wishes of the minister. If indeed the minister wants individuals to save in a way that would also help in nation-building, issues such as inflation, current account deficit and fiscal deficit have to be addressed so that faith in fiat currency returns.

* * |

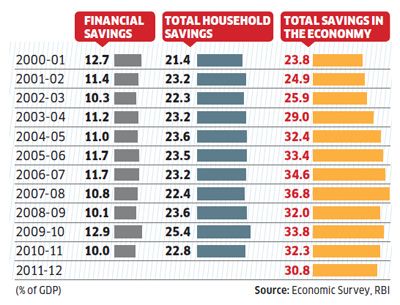

Savings Go Down

Indians, who were once among the top savers in the world — next only to China — are set to save less this year.

Thanks to a slowdown, accompanied by high inflation and consumer spending, India's savings are set to touch a decade low.

Though savings have been falling for the past few years, what is hurting theeconomy more is the decline in financial savings — savers, particularly the household sector, now prefer to park more savings in physical assets such as residential properties and other valuables.

A slowdown in savings is also a concern for policy makers, as growth will have to be financed by foreign inflows which could add to the external sector pressures

http://economictimes.indiatimes.com/news/economy/finance/only-money-in-circulation-can-lift-the-economy/articleshow/18474563.cms

13 FEB, 2013, 05.00AM IST,

Pay the price for democracy to fight corruption

We can't wish away the problem if we want to seriously tackle corruption. We love our democracy and have reason to be proud of it. Now we must figure out how to pay for it.

By, Janmejaya K SinhaThe brutal rape and senseless killing of the girl in Delhi pushed the issue of corruption of the headlines from the Indian electronic and print media. The frustration around corruption, both big and small, spawned the Anna Hazare movement and also managed to provide Arvind Kejriwal a political platform. However, the discussion has been marked by frustration, hyperbole, cynicism and great naivete.

There has been a lot of acrimony and no real introspection. Everyone has been painted vile: be it politicians, bureaucrats, businessman, media, and even the judiciary. Some of the description is no doubt true, but what is the root cause? It appears as if the nation has lost character suddenly. I don't agree with that.

In fact, no one has really tried to establish the linkage of corruption with something all Indians hold very dear: our democracy.

Let us compare the cost of Indian democracy to the cost of democracy in the US. In 2012, $6.2 billion was spent in the US by candidates fighting elections, including the presidential candidates. In rupee terms, this amounts to something like Rs 35,000 crore. The presidential election alone cost about $3 billion (Rs 16,000 crore), with the two candidates officially raising about $1.2 billion (Rs 6,000 crore). Now, consider the US has about 300 million people, two political parties, higher levels of literacy, two main languages and much easier communication.

India has close to 1.2 billion people, a more complex electoral system with 40 political parties, 22 languages and higher barriers to communication. So how much does our democracy cost us? This is what I call the corruption calculus. In this piece, I intend to start a debate on what this cost may be for us and how we fund it.

If a Senate seat in the US costs about $10 million to contest, it provides a good benchmark to work with. We have 543 parliamentary seats in India. If we were to assume the same figure of $10 million, it would translate into Rs 55 crore per seat. A bottom-up build-up can easily add up to that number. Each parliamentary seat represents, on average, more than 2.2 million people. Parties conduct a lot of activities to reach people and win their vote. They issue advertisements in newspapers or on television, put up hoardings, engage party workers, organise rallies, transport people to rallies, print brochures, send out letters and the like. Given a new year card costs Rs 50, and even a cheap printed brochure costs more than Rs 5, it would not be unreasonable to assume that each serious party spends about Rs 80 to reach one person.

If there are three serious parties per constituency, then all the parties are collectively spending around Rs 240 per person in every constituency. This adds up to about Rs 50 crore per parliamentary seat. If we then talk about 545 seats in Parliament, the Lok Sabha elections cost India about Rs 30,000 crore to contest.

http://economictimes.indiatimes.com/opinion/comments-analysis/pay-the-price-for-democracy-to-fight-corruption/articleshow/18472987.cms

A look at India's last five annual budgets

By Aditya KalraFEBRUARY 6, 2013

The countdown has begun for the biggest business and economic event of the year, the release of India's annual budget at the end of February, and Finance Minister P. Chidambaram has a tough job on his hands. With general elections a year away, he must please voters, boost growth and control deficits.

In the last five years, the finance minister has always relaxed income tax slabs — by either increasing the basic exemption limit or widening the tax slabs. As far as markets go, the 2009 budget day was the worst for stocks as the index fell around 950 points during trade. However, the focus has always been on the government's fiscal deficit targets, which have hovered around the 5 percent mark in recent years.

As India's economy battles slowing growth, investors will take cues from Chidambaram's plans to rein in spending and boost growth. Here's a look at budgets between 2008 and 2012 — the hits, the misses and how they affected the common man.

2012

FINANCE MINISTER: Pranab Mukherjee

KEY HIGHLIGHTS

- India projects a decline in the fiscal deficit to 5.1 percent of GDP in 2012/13. GDP expected to grow at 7.6 percent.

- Controversial proposal to retrospectively tax cross-border transactions in which the underlying assets are located in India. The move amounts to a push to get foreign companies that have invested millions in India to pay more taxes. Or in India's words, it's supposed to fight "counter aggressive tax avoidance schemes".

- Service tax rate raised to 12 percent from 10 percent, double basic customs duty on gold.

- No change in corporate tax rates. Personal Taxation: minimum threshold of income not chargeable to tax increased to 200,000 rupees. The 30 percent tax slab applicable on income above 10,00,000 rupees.

- Moody's said: "mildly negative" for India's credit rating. India's budget lacks new solutions to address its fiscal constraints and is credit negative for the sovereign.

- Standard & Poor's said the budget was "mildly negative" for India's credit rating, noting that the timing remained uncertain for long-awaited reforms.

- The BSE Sensex fell 210 points (1.2 percent) to close at 17,466 as the budget was seen as too modest for a corporate sector looking for more concessions. During trade, the index fell nearly 250 points.

FINANCE MINISTER: Pranab Mukherjee

KEY HIGHLIGHTS

- Social spending to rise by 17 percent in 2011/12, helping millions of Indians. Fiscal deficit seen at 4.6 percent of GDP in 2011/12.

- Spending on infrastructure increased by 23 percent.

- Service tax rate kept at 10 percent, but scope widened. Minimum Alternate Tax (MAT) raised to 18.5 percent from 18 percent.

- Personal income tax exemption limit raised to 180,000 rupees. Surcharge on domestic companies reduced to 5 percent.

- Standard & Poor's said India's fiscal deficit target for 2011/12 may be bit difficult to attain given upside risks to oil subsidy and wage bill under the social employment programmes.

- The BSE Sensex ended up 0.69 percent at 17,823.40 points after rising as much as 3.4 percent after the budget was unveiled.

2010

FINANCE MINISTER: Pranab MukherjeeKEY HIGHLIGHTS

- India plans record levels of borrowing for 2010/11 and counts on big growth to help cut its fiscal deficit to 5.5 percent of GDP.

- Excise duty raised on petrol, diesel by 1 rupee per litre. Excise duty cuts on cement, cement products and large cars partially rolled back.

- Minimum alternate tax rate raised to 18 percent from 15 percent. Service tax rate kept unchanged at 10 percent.

- Corporate tax rate unchanged. Personal income tax slabs widened.

- Standard & Poor's: "We believe the steps announced could signal a turning point that reverses the recent deterioration in India's fiscal position."

- The BSE Sensex rose as much as 2.6 percent after the budget before paring gains. The index ended with gains of 175.35 points (1.08 percent) at 16,429.55.

2009

FINANCE MINISTER: Pranab MukherjeeKEY HIGHLIGHTS

- Plans outlined to speed infrastructure development and increase spending for farmers and the poor. Additional spending to push the fiscal deficit to a 16-year high of 6.8 percent of GDP, the finance minister said.

- Minimum Alternate Tax raised to 15 percent from 10 percent. Fringe benefit tax scrapped.

- Corporate tax rates unchanged. Personal income tax exemption for senior citizens increased by 15,000 rupees; raised by 10,000 rupees for others.

- Standard & Poor's said India's BBB-minus sovereign rating does not face any significant rating pressure despite a sharply higher fiscal deficit unveiled by the government.

- Fitch said that, given India's ever widening physical and social infrastructure deficit, the expectations that the budget for fiscal 2010 would provide a boost to the sector were very high.

- After falling more than 950 points during trade, the BSE Sensex ended with an 870-point loss(5.8 percent) to close at 14,043.40. It was the index's biggest drop in six months.

2008

Finance Minister: P. ChidambaramKEY HIGHLIGHTS

- Fiscal deficit for 2008-09 seen at 2.5 percent of GDP. Ahead of the 2009 elections, the government proposed to waive 600 billion rupees of bank loans to farmers.

- The budget raised the short-term capital gains tax, when an investment is sold for profit before one year, to 15 percent from 10 percent.

- Excise duty on pharmaceuticals sector cut to 8 percent; Duty on small and hybrid cars to be cut. Six percent duty on petrol and diesel abolished and replaced with specific duty of 1.35 rupees per litre.

- Corporate tax rates unchanged. Income tax threshold raised to 150,000 rupees.

- Standard & Poor's said the budget was largely in line with expectations but more work needed to be done for upgrading ratings.

- Fitch Ratings said India needs to do more for fiscal improvement to catch up with its peer group.

- The BSE Sensex ended down 246 points(1.4 percent) at 17,578.72 after falling as much as 3.2 percent.

- (You can follow Aditya on Twitter @adityayk)

NEXT POST »

More From Reuters

- Hollande urged to cut public spending(Financial Times)

- Tea Party dim bulbs go after renewable energy standard in Kansas (Grist Magazine)

- Sarah Palin Jabs Washington Post Over Fake Al Jazeera Story (The Wrap)

- When It Comes to Online Hispanics, the Internet Is Blue (Hispanic Online Marketing)

- iPhones And Americans: How Consumer Electronics Became A… (Fast Company)

No comments:

Post a Comment