Why the rich should not be taxed more!Ghost of GAAR buried: Chidambaram,Consumers across the country are likely to be burdened with another round of hike in prices including electricity tariffs, CNG powered transport, households using piped gas!

Troubled Galaxy Destroyed Dreams, Chapter: 836

Palash Biswas

Mobile: 919903717833

Skype ID: palash.biswas44

What does tax reform mean in India? More stimulus , more concession for the rich as well as super rich as they never belong to the excluded communities selected for systematic ethnic cleansing! Pre budget debate as well as policy making is focused on one point agenda that the rich in India should not be taxed as it would stall tax reforms. We have witnessed the GAAR episode. We have been witnessing continuous balance of payment crisis just because of bygone tax in lacs and sustained fiscal deficit due to foreign debt to balance the payment. Finance Minister P Chidambaram is proving himself industry friend unprecedented at the cost of the mango people in the banana republic.Asserting that India continues to be a "very good" investment destination, Urban Development Minister Kamal Nath today said the government would roll out more policy reforms in the next couple of months.Nath also said stress and distress are in Western economies, not in India. He is leading the Indian delegation at the World Economic Forum ( WEF) annual meet.

India has a well developed tax structure. The power to levy taxes and duties is distributed among the three tiers of Government, in accordance with the provisions of the Indian Constitution. The main taxes/duties that the Union Government is empowered to levy are:- Income Tax (except tax on agricultural income, which the State Governments can levy), Customs duties, Central Excise and Sales Tax and Service Tax. The principal taxes levied by the State Governments are:- Sales Tax (tax on intra-State sale of goods), Stamp Duty (duty on transfer of property), State Excise (duty on manufacture of alcohol), Land Revenue (levy on land used for agricultural/non-agricultural purposes), Duty on Entertainment and Tax on Professions & Callings. The Local Bodies are empowered to levy tax on properties (buildings, etc.), Octroi (tax on entry of goods for use/consumption within areas of the Local Bodies), Tax on Markets and Tax/User Charges for utilities like water supply, drainage, etc.

Major global companies including Novartis, BAE Systems and Philips today expressed interest in expanding their businesses in India. Heads of the multi-national companies have shown keenness to shore up their operations in India during their meetings with Commerce and Industry Minister Anand Sharma, who is based in Davos now to participate in the annual WEF event.What does it mean? do you need any explaination? Just read the policy statements. Here you are!

"Watch the upcoming budget closely: it will prove that we mean business."

With those upbeat words – and a pledge to restore the Indian economy to a higher growth orbit next year – Finance Minister P Chidambaram, accompanied by a high-power Finance Ministry delegation, wooed investors in Hong Kong on Tuesday.The First Post reports.

At a closed-door session with investors – representing sovereign funds, wealth funds and asset management companies – Chidambaram hard-sold the India story, and sought to allay investors' concerns that the UPA government lacked the political will to do what it takes.

The Minister said he had been able to "bury the ghost" of GAAR. Reuters

Some of the investors who attended the investment roadshow that Chidambaram and his All-Star team got on the road ahead of Budget 2013 told Firstpost on condition of anonymity that the Minister was repeatedly asked about the government's ability to "stay the course" on unpopular but necessary reforms.

Investors also quizzed Chidambaram on the prospects of a sovereign rating downgrade if the government overshot its deficit targets. He, in turn, assured them that he would stick to his targets – no matter what.

"Under no circumstance will I agree to a breach of the fiscal deficit target of 5.3 percent of GDP," Chidambaram told mediapersons later.

The steps that the government had taken in recent weeks – such as the diesel price deregulation – had "assured everybody that there will not be a rating downgrade," he added. "They were concerned about our ability to stay the course after we announced the decisions. They are happy that we stayed the course after announcing FDI in multi-brand retail."

Investors' concerns that fuel price rationalisation – which was an important componenent of fiscal consolidation – would not be implemented had been sufficiently allayed, Chidambaram said. "Even the small steps we have taken have reassured them… Each of the measures has boosted their confidence in the Indian economy," he added.

Investors also pressed Chidambaram for clarity on the GAAR provisions, even though their implementation has been put off until 2016.The Minister said he had been able to "bury the ghost" of GAAR. "I explained to investors all the measures we have undertaken on GAAR, and pointed out that the stock market had received the proposals well. There is universal acknowledgement that we have handled the GAAR situation fairly effectively," he claimed.

The Indian economy, Chidambaram said, is "undeniably growing faster"; only China and Indonesia were growing at a faster pace. Yet, he noted, this wasn't sufficient, and there was a compelling need to accelerate growth."

The first step towards getting the growth engine revving was fiscal consolidation and showcasing a commitment to fiscal prudence. "We will achieve the targeted fiscal deficit of 5.3 percent of GDP this year, and for the next year, I will budget for a fiscal deficit of no more than 4.8 per cent next year."

GDP growth in 2013 would be between 6 and 7 percent, particularly since there had been a revival of investor confidence. "If investment gathers pace, we should get back to our growth rate of 8 per cent," Chidambaram said. "India's potential growth rate is above 8 per cent above. We have done it before. We will do it again."

Flashes of the petulance that Chidambaram has exhibited in recent times with the RBI, which has not heeded hints to lower interest rates, were again visible at the media briefing. Asked about the prospects for lower interest rates given that the RBI's focus on fighting inflation, Chidambaram said: "I don't manage the RBI. I merely convey the views of the government. It is for the RBI to take a call. Our stated position is that the RBI must balance between the need to stimulate growth and contain inflation."

"Policy reforms will continue and we will roll out more (reforms) in next couple of months," Kamal Nath, who is also in charge of Parliamentary Affairs, told PTI here.

In response to a query on whether the government would continue with policy measures for economic reforms on top of the recent decisions, he said" "Yes we are continuing."

Nath, who was instrumental in pushing the FDI reforms in the Parliament last month, stressed that the country is an attractive investment destination.

"India continues to be a very good investment destination and we have no stress or distress in our economy. The stress and distress lie in the western countries today. India is adapting to growth realities and the US and Europe are in distress," the Minister said.

In recent months, the government has unleashed a wave of reforms to bolster the sagging economic growth, which is expected to be around 5.7 per cent in the current financial year ending March 31, 2013.

The major reform measures include liberalisation of FDI norms in multi-brand retail and aviation sectors and partial de-regulation of diesel prices. Besides, steps have been initiated to keep subsidies under control.

India has buried the "ghost" of GAAR, Finance Minister P. Chidambaram said on Tuesday asserting that there is no threat of a rating downgrade in view of key economic decisions like allowing FDI in multi-brand retail and hiking fuel prices.Efforts to widen the tax base and increase revenues will continue, Finance Minister P Chidambaram said on Wednesday.He said there is revival of investor interest in India as a result of a number of measures taken by the government since September 2012.

The biggest threat to reforms in India is an unstable government at the Centre after 2014, finance minister P Chidambaram told investors and analysts in Singapore on Wednesday as he laid defined the broad contours of the economic agenda in the coming months.The Mint reports.

"The FM hopes to pass the Insurance Bill and the Pension Bill in the budget session of Parliament. He mentioned that behind the noise, there were quiet negotiations with the opposition parties and support from them," said a research note Bank of American Merrill Lynch that hosted a meeting between Chidambaram and investors in Singapore.

The Goods and Services Tax (GST) is unlikely to be passed by April 2013. "But the FM hopes to introduce the Bill in the monsoon session and pass it in the winter session in December this year," the report said.

Billed as India's biggest tax reform initiative, GST promises to stitch together a common national market by replacing a welter of local levies such as value-added tax (VAT) and octroi by a single tax.

"If there is a consensus with the states on these issues, the FM is hoping to move the GST legislation in the monsoon session of Parliament and pass the Bill in the winter session," the report said.

As reported in HT on January 22, Chidambaram promised a stable tax regime maintaining that efforts would be made to widen the tax base.

The finance minister was confident of keeping the fiscal deficit-broadly refers to the amount of money that the government borrows to fund its expenses — for this year at 5.3% of GDP.

Ahead of next week's monetary policy, Finance Minister P. Chidambaram, on Tuesday, said the Reserve Bank of India (RBI) must strike a balance between the needs of pushing growth and controlling inflation.

"I don't manage the RBI. I just convey the views of the government. It is for the RBI to take a call.

"Our stated position is that the RBI must balance between the needs of stimulating growth and containing inflation," he told PTI.

The RBI is slated to announce its third quarter review of monetary policy on January 29 amid demands by industry that it should lower interest rates to boost industrial output, which contracted by 0.1 per cent in November.

Before announcing the policy, the RBI Governor holds a customary meeting with the Finance Minister.

In order to contain inflation, the RBI has refrained from lowering interest rates despite nudging by Finance and Commerce ministries that it should take steps to address concerns on growth.

Inflation based on wholesale prices declined to a three-year low of 7.18 per cent in December. However, retail inflation rose for the third successive month in December to 10.56 per cent.

Mind you,Consumers across the country are likely to be burdened with another round of hike in prices including electricity tariffs, CNG powered transport, households using piped gas as the Petroleum and Natural Gas Ministry has moved the Cabinet for nearly doubling the price of domestically sold gas to $8 to 8.5 per million British thermal unit from the present $4.2 mmbtu, a move that could put an additional financial burden of nearly Rs. 7000 to Rs. 8000 crore on the common man.The Hindu reports.

Oil Ministry has moved a Cabinet note for nearly doubling the price of natural gas produced by state-owned ONGCBSE -1.14 % and OIL to $ 8-8.5 per million British thermal unit in the current year itself and for Reliance IndustriesBSE 0.31 % from April 2014.

The Ministry in a draft Cabinet note proposed accepting in toto the Rangarajan Committee recommendation of pricing domestically produced natural gas at an average of international hub prices and cost of imported LNG instead of present mechanism of market discovery.

Sources said ministry wants the pricing formula proposed by the panel to apply to all forms of natural gas - conventional, shale and coal-bed methane (CBM). Also, the price determined shall be applicable to all consuming sectors uniformly.

It, they said, wanted the new pricing guidelines to apply from 2013 itself on all domestically produced gas barring cases where it is either governed by a definite formula prescribed in the Production Sharing Contract (PSC) or the government had previously fixed a tenure for the same.

This essentially meant that RILBSE 0.31 % would get the new price only from April 1, 2014 upon expiry of the fixed five-year term of current rate of $ 4.205 per million British thermal unit.

State-owned Oil and Natural GasBSE -1.14 % Corp (ONGC) and Oil India LtdBSE -4.91 % (OIL) can, however, get the new rates this year itself for gas they produce from fields given to them on nomination basis by the government. Gas from nominated fields, called APM gas, is currently priced at $ 4.2 per mmBtu.

The Rangarajan panel suggested rates may also not apply to BG Group-operated Panna/Mukta and Tapti fields in the western offshore as the current rates of $ 5.57-5.73 per mmBtu for the fuel produced from these are derived from a pre-defined formula detailed in the PSC.

However, CairnBSE -1.32 % India's eastern offshore Ravva gas, which is currently priced at $ 3.5-4.3 per mmBtu, may be revised as per the committee recommendations.

Sources said the ministry said the Rangarajan panel report needs to be accepted so that domestically produced natural gas prices are fixed in a fair manner and in a way that incentivises production.

The panel had suggested taking a weighted average of the US, Europe and Japanese gas hubs or market price and then averaging it with the net imported price of liquefied natural gas (LNG) to give sale price of domestically produced gas.

Taking last year's publicly available consumption numbers and the prevailing price of gas in the three markets, the formula suggested by the Rangarajan committee gives $ 8-8.5 per mmBtu as the price of domestic gas.

Citing the recommendations of the recently set up Rangarajan Committee, which had come out with a roadmap for gas pricing, the Petroleum Ministry has sought an immediate hike in the price of gas sold by state-run Oil and Natural Gas Corporation (ONGC) and Oil India Limited (OIL) from $4.2 mmbtu to $8-8.5 mmbtu. However, in case of Mukesh Ambani-owned Reliance Industries Limited (RIL), which has been pushing for nearly tripling the gas price to around $13 mmbtu, the price hike will take effect from April 2014, the deadline set by the Empowered Group of Ministers (EGoM) in 2009.

By moving to push for almost double the hike in gas prices, the Petroleum Ministry has gone with the Rangarajan Committee recommendations for pricing domestically produced natural gas at an average of international hub prices and cost of imported LNG instead of present mechanism of market discovery. This despite plea by the Association of Power Producers (APP) that the Japanese import price formula suggested by the Rangarajan Committee should be removed from the hub prices as Japan LNG prices have been historically been much higher than the global market and this would distort the gas pricing. The APP has also contended that this would put an additional burden of Rs. 7000 to Rs. 8000 crore on the consumers.

In fact, government sources said the Petroleum Ministry has pitched that the pricing formula proposed by the panel be applied to all forms of natural gas - conventional, shale and coal-bed methane (CBM). Also, the price determined shall be applicable to all consuming sectors uniformly. The Ministry was keen on putting the recommendations into immediate effect and has strongly favoured that new prices should be applied without any further delay on all domestically produced gas barring cases where it is either governed by a definite formula prescribed in the Production Sharing Contract (PSC) or the government had previously fixed a deadline for the same.

Such a move would make gas produced from the KG basin bock of RIL automatically disqualified from revision of prices as under the EGoM approved guidelines, KG basin gas prices would be revised only after April 2014. ONGC and OIL will be the biggest beneficiaries of this government largesse this year for gas they produce from fields given to them on nomination basis by the government. Gas from nominated fields, called APM gas, is currently priced at $4.2 per mmBtu. The Rangarajan panel also suggested that rates may also not apply to BG Group-operated Panna/Mukta and Tapti fields in the Western offshore as the current rates of $5.57-5.73 per mmBtu for the fuel produced from these are derived from a pre-defined formula detailed in the PSC. However, Cairn India's eastern offshore Ravva gas, which is currently priced at $3.5-4.3 per mmBtu, may stand revised as per the latest recommendations.

The Rangarajan panel had suggested taking a weighted average of the US, Europe and Japanese gas hubs or market price and then averaging it with the net imported price of liquefied natural gas (LNG) to give sale price of domestically produced gas. Taking last year's publicly available consumption numbers and the prevailing price of gas in the three markets, the formula suggested by the Rangarajan committee gives $8-8.5 per mmBtu as the price of domestic gas.

Mr. Chidambaram was also hopeful that fiscal deficit will be contained within the targeted 5.3 per cent of the GDP this fiscal and trimmed to 4.8 per cent in the next. Growth is likely to climb to 6-7 per cent from 5.7 per cent expected in the current year, he said.

"There is universal acknowledgement that we have handled the GAAR situation fairly effectively and buried the ghost that GAAR will be some kind of a monster," he told PTI in an interview.

Here on a day's visit for an investor conference, the Finance Minister said as expected investors raised issues relating to the controversial provision of GAAR that was introduced in the 2012-13 Budget by his predecessor.

The General Anti-Avoidance Rules (GAAR) gave unbridled powers to taxmen to check evasion of taxes by foreign investors that created huge apprehensions among investors.

Last week, Mr. Chidambaram announced that GAAR implementation has been postponed by two years to 2016.

"On specific questions on GAAR and I took some time in explaining all the measures we have made to GAAR and told them how market has received it very well here. There is universal acknowledgement that we have handled the GAAR situation fairly effectively and buried the ghost that GAAR will be some kind of a monster," he said.

Kicking off his campaign to woo investment, Mr. Chidambaram met over 200 top investors at the "India for Investment Conference" organised by the Citibank and BNP Paribas.

He made a strong case for their investment assuring that all their concerns were being addressed and that the government has taken all measures including to contain fiscal deficit.

"It is a very well attended meeting. Virtually everybody who is anybody in the financial sector was here including wealth funds, sovereign funds, banks asset management companies. It gave me an opportunity to explain the economic situation in India, the steps we are taking to put the economy on high growth path," he said.

Mr. Chidambaram, who will be in Singapore on Wednesday on a similar mission, said India continues to post growth even now.

"We are undeniably growing faster," he said pointing that out only China and Indonesia are ahead of India.

"But this growth is not sufficient for us. We need to accelerate it. So I told them steps we are taking to accelerate growth," he said.

He said the first step in that direction is fiscal consolidation and commitment to the path of fiscal prudence.

"At that at the end of this year, we will achieve the target of 5.3 percent of fiscal deficit and next year I will budget for fiscal deficit no more than 4.8 percent," he said.

He said he has also explained to the international investors the number of measures taken in this regard.

"I thought it was a fruitful conference. I could get a sense of the concerns of investors. Happily many of the concerns were addressed in the last three of four months," he said.

Nevertheless,India's Foreign Direct Investment (FDI) inflows declined to a nearly two-year low of USD 1.05 billion in November 2012, mainly due to global economic uncertainties.

In November 2011, the country had attracted FDI worth USD 2.53 billion.

For the April-November period 2012-13, the inflows have declined by about 31 per cent to USD 15.84 billion, from USD 22.83 billion in the year-ago period, a senior official in the Department of Industrial Policy and Promotion (DIPP) told PTI.

According to experts, the global economic situation is the main reason for decline in the inflows.

"The global economic slowdown and lack of political consensus on FDI related matters are the reasons for decline," said Krishan Malhotra, Head of Tax and expert on FDI with corporate law firm Amarchand & Mangaldas.

Sectors which received large FDI inflows during the eight months of the current fiscal include services (USD 3.63 billion), hotel and tourism (USD 3.13 billion), metallurgical (USD 1.26 billion), construction (USD 1.01 billion) and automobile (USD 760 million), the official added.

India received maximum FDI from Mauritius (USD 7.2 billion), Japan (USD 1.56 billion), Singapore (USD 1.5 billion) the Netherlands (USD 1.09 billion) and the UK (USD 615 million).

The previous low was recorded in January 2011 when the FDI inflows slipped to USD 1.04 billion.

The inflows had aggregated to USD 36.50 billion in 2011-12 against USD 19.42 billion in 2010-11 and USD 25.83 billion in 2009-10.

In Singapore,Wooing over 300 city-based investors on the second leg of his east Asia tour, he said India is poised to grow at over 8 per cent from fiscal 2015-16 onwards.

"...efforts to keep on increasing the tax base will continue ... so that the tax revenue to the proportion of the GDP will also remain robust," he was quoted as saying by Sanjiv Bhasin, General Manager and CEO of DBS Bank, India.

The government, Minister said, was taking steps to bring down the fiscal deficit to 3 per cent of the Gross Domestic Product (GDP) in the next three to four years.

Mr. Chidambaram had on Tuesday told investors in Hong Kong that he was committed to keeping fiscal deficit to 5.3 per cent of the GDP in the current fiscal and reduce it further to 4.8 per cent in 2013-14.

As regards growth, the Minister was reported to have told investors that "India has fumbled, but so has most other economies worldwide".

The growth, Mr. Chidambaram had earlier said, was not likely to be below 5.7 per cent in 2012-13 and would improve to about 6-7 per cent in the next fiscal. Indian economy grew by 6.5 per cent in 2012-13.

The Minister, according to investors attending the meeting, has said that the Indian government was making efforts to put economy back on track.

In his over two-hour long interaction with investors, Mr. Chidambaram spoke on host of issues including fiscal deficit, current account deficit, expenditure management and slowing economy.

Mr. Chidambaram assured the investors that savings from subsidies would help bring down fiscal deficit, said Bhasin.

Among other things, the Minister said that efforts were on to ensure that the savings rate, which was as high as 35-36 per cent of the GDP, is raised to the same level.

Mr. Chidambaram also highlighted India's success in many fields including the Aadhar platform, and the country becoming the world's largest rice exporter as well as substantial exporter of wheat.

He said plans were in place to spread the green revolution to other states that have not been impacted by the farm sector programmes of the government.

The US Congress voted for raising taxes on the wealthiest Americans as part of a resolution of the crisis over the fiscal cliff. The Economist spooked the deal saying President Barack Obama had failed to clear up the US economy's fundamental fiscal trouble, and that he and the Republicans were building Brussels on the Potomac. The world will have to wait to see if the prognosis comes true.India, unlike the US, does not face the calamity of the fiscal cliff. But government's finances are in a mess. And we need to look at ways to raise more revenues to bring the economy to a better shape. Two proposals are being hotly debated now in the run up to the Budget. One is to have an inheritance tax and the other a higher tax rate for the super-rich. Both are unsound.The Economic Times reports.Agreed, many countries are raising income tax rates in a desperate bid to garner more resources. In the US, billionaire investor Warren Buffet supported the idea of a higher tax on the super rich, saying he was paying a lower rate of tax than his own employees due to a slew of exemptions. Similarly, France plans to impose a substantial tax on the super-rich, a move that prompted French actor Gerard Depardieu to take up citizenship in Russia. The point is high income tax rates on the wealthy can discourage work and investment. It would be imprudent for India to take a page from these countries. That would be one step back on tax reform.

Contrarily,India's super-rich cannot treat extreme wealth as personal wealth, Wipro chairman Azim Premji has said, calling for higher consciousness among India's wealthy. In such a poor country, there is a legitimacy in taxing the super-rich, he added.The Wipro chairman was reacting to a report by Oxfam International, which says the poorest people in the world could be lifted out of poverty several times over should the richest 100 billionaires give away the money they made last year. The data saddened him, Mr Premji told NDTV on the sidelines of the six-day long World Economic Forum meet, which kicked off yesterday in the idyllic ski town of Davos, Switzerland. Profit NDTV reports.

The very wealthy, said one of India's richest men, "have a responsibility for that wealth, and not just a legacy to leave it to their family". He, however, said that the base of income and wealth must be increased rather than redistributing wealth.

"...wealthy people should consider it as part of their obligation ... the more they think so, the longer they are going to survive in their positions. Otherwise, the forces of socialism will overtake them," Mr Premji, who is also a noted philanthropist, added.

The pandemic scourge of economic disparity has been in the news now after eminent Indian economists asked the government to levy higher taxes on the super-rich. However, captains of India Inc., including HSBC's country head for India and director of Asia Pacific Naina Lal Kidwai and Godrej Industries chairman Adi Godrej, asked the government to not raise taxes on the extremely wealthy as it would discourage entrepreneurship.

The reforms initiated by the UPA government in recent months, Mr Premji said, were "too little too late". "There is a sense of urgency and healthy panic within the government, but the reform push may be too little too late as India has lost a lot of economic momentum in last 2-3 years," he added.

he government's recent push for multi-brand retail foreign direct investment, he said, was "a good policy, but there are more important priorities to ... get moving forward". Mr Premji said it was not worthwhile to have lost two weeks of Parliament work on it. "I don't think there is a need to do all kinds of new things... you just need to execute and need to ensure higher standards of governance."

He was optimistic about the state of the world economy, pointing out that the US had been showing positive signs of late. "...And the US drives a lot of the world scene," Mr Premji said. "China is also not doing as bad as has been made out. They'll still end up probably with an 8 per cent growth rate ... The good thing is that there is a major shift taking place in the country from investments to consumerism to fillip demand."

The Middle and Far East look reasonably good with an expected 4-5 per cent growth rate, Mr Premji said. However, concerns remain from the developments in Europe, although he lauded Greece for launching "constructive reforms".

"Spain is facing very hard times in unemployment ... but overall, the latest forecast I read by Gartner (a research firm) of the services growth for the world this year was somewhere at 5-6 per cent, which is decent," he added.

But Economic Times opines.Lets not forget that estate duty flopped in India. Introduced in 1953, the law was complex and riddled with exemptions. It was scrapped in 1985. Curiously, the UPA government has offered reasons on why the tax was abolished. One, estate duty yielded small change despite a progressive rate schedule. The percentage of estate duty to gross tax collections slumped from 0.22 % in 1972-73 to 0.13% in 1981-82. Two, the levy entailed both high administrative costs for the exchequer and compliance costs for taxpayers. Three, wealth tax and estate duty were levied on the same property -- one was imposed before the person's death and the other after her death. Naturally, taxpayers were unhappy with the huge burden.

Yet, a few months ago finance minister P Chidambaram called for a debate on inheritance tax. And economists also came out in support of the levy during the pre-budget discussions with the FM. Its pros and cons are well chronicled. Votaries say an estate tax brings about inter-generational equity - so that children of the rich enjoy attenuated advantage in life compared to their peers who are not so privileged. The counter argument is that the levy penalizes savings and investment and discourages capital formation. Worse, it encourages tax avoidance through the creation of trusts and shell companies to which the assets can be transferred. Past research in the US showed that inheritance tax was not just an inefficient levy, but also created a large wasteful estate planning and avoidance industry. Should we let the same happen in India? The answer is no.

On the contrary, it is quite possible that India can attract tax tourists from high estate tax countries provided, of course, the government fixes many things like the creaky infrastructure and makes the legal framework sound. But that's another story.

Alternately, can't the government raise the tax rate for the super-rich. It could impose a rate higher than the peak income tax rate of 30% or clamp a surcharge on incomes above a certain threshold as was done in the past. Technically, there is no bar. But multiple tax rates distort the tax structure. It also goes against the grain of tax reform. Many wealthy Indians are said to have stashed their undisclosed wealth in Swiss banks and other tax havens to escape high taxes here. Clearly, we should not fuel the black economy by increasing tax rates.

Peter Morgan,Freelance macroeconomist writes for Huffington Post,Taxing the Rich Will Not Solve the Problem:

I have recently read a number of articles stating the solution to the economic crisis is merely to tax the rich. However, I doubt it is that simple and it may in fact create more problems than it solves. I provide my justification below, by explaining the use of the money held by the "rich" and how this benefits the rest of the economy.

So what about:

The money they have in the bank?

Savings in banks provide investment into the economy, when banks lend the funds deposited. This lending enables businesses to borrow money to start up, pay staff and cover overheads. It also enables homebuyers to arrange mortgages and it works as short term credit for borrowers, when it is lent out through credit cards. This money provides a service when it is invested, by taxing the rich the money will be taken from banks, reducing their ability to lend in the future. This would do tremendous damage to the economy and labour market.

The money they have in shares?

Share ownership is another investment favoured by the rich. They receive dividends and potential increases in share value as incentive to buy shares. Although a huge amount of money is invested in shares, making the rich sell their shares to pay tax will have a negative impact on the economy. If shares were sold at the magnitude that would be required to pay off public sector debt, the share price would plummet. By owning shares on a huge scale, the rich provide an artificial value to share prices. This would no longer exist if they were forced to sell them on the level needed to balance the national debt. This would have a catastrophic effect on private sector pensions, which are largely funded by share investment. It could push thousands, perhaps millions of pensioners into poverty.

The money they have in assets like property, cars and yachts?

In the same way the share price drops when shares are sold on mass, asset prices will fall when sold on mass too. If the wealthy sector of society were expected to sell off their assets to "pay off" the public deficit in one go, the price they would receive for the assets would fall dramatically. It would become a buyer's market. Who would buy these assets anyway? If you are taxing all of the people who have the means to buy expensive assets, who will have the money needed to buy them? The situation is not simply a matter of the rich having assets worth X amount of money, but who has X amount of money to buy the assets from the rich? And more importantly do they want to buy them?

The money they have in cash?

Money held in cash could be taken in tax, however, even if the money is seemingly doing nothing, it is doing something. Money not used in the economy reduces the price of goods, which would otherwise increase demand pushing up prices. In short, money not spent prevents inflation, which makes the cost of goods higher. As inflation is currently high it would not be advisable to take this money and spend it. If this was done the price of goods would rise and would be counterproductive to reducing poverty, which I assume is the intention of the taxes.

Conclusion.

There is one underlying principle in the above points. Money always does something. It is always being used to enable the functions an economy needs. By taxing the rich, all that is achieved is a transfer of wealth from the private sector to the public sector. Most economists would argue money in the private sector is "better" at increasing output and providing employment. It also has to be said, if the public sector has racked up this level of debt. Surely it is not effective at managing money? Taxing the rich is no different from cutting government expenditure. It will simply take money working in the economy out, to reduce the deficit. This action will have the same consequences to employment, investment and services that public sector cuts have.

http://www.huffingtonpost.com/peter-morgan/taxing-the-rich_b_1131020.html

Why the rich should pay more taxes

This piece, like my taxes, is just a bit late. For non-American readers, I should explain that income taxes are due on April 15. Non-American readers may also be utterly astonished at the arguments made below. Could Americans really be so lacking in common sense? Believe me, they could.

--Mark Rosenfelder

For more than a century it's been generally recognized that the best taxes (admittedly this is an expression reminiscent of "the most pleasant death" or "the funniest Family Circus cartoon") are progressive-- that is, proportionate to income.

Lately, however, it's become fashionable to question this. Various Republican leaders have trotted out the idea of a flat tax, meaning a fixed percentage of income tax levied on everyone. And in their hearts they may be anxious to emulate Maggie Thatcher's poll tax-- a single amount that everyone must pay.

Isn't that more fair? Shouldn't everyone pay the same amount?

In a word-- no. It's not more fair; it's appallingly unfair. Why? The rich should pay more taxes, because the rich get more from the government.

Consider defense, for example, which makes up 20% of the budget. Defending the country benefits everyone; but it benefits the rich more, because they have more to defend. It's the same principle as insurance: if you have a bigger house or a fancier car, you pay more to insure it.

Social security payments, which make up another 20% of the budget, are dependent on income-- if you've put more into the system, you get higher payments when you retire.

Investments in the nation's infrastructure-- transportation, education, research & development, energy, police subsidies, the courts, etc.-- again are more useful the more you have. The interstates and airports benefit interstate commerce and people who can travel, not ghetto dwellers. Energy is used disproportionately by the rich and by industry.

As for public education, the better public schools are the ones attended by the moderately well off. The very well off ship their offspring off to private schools; but it is their companies that benefit from a well-educated public. (If you don't think that's a benefit, go start up an engineering firm, or even a factory, in El Salvador. Or Watts.)

The FDIC and the S&L bailout obviously most benefit investors and large depositors. A neat example: a smooth operator bought a failing S&L for $350 million, then received $2 billion from the government to help resurrect it.

Beyond all this, the federal budget is top-heavy with corporate welfare. Counting tax breaks and expenditures, corporations and the rich snuffle up over $400 billion a year-- compare that to the $1400 budget, or the $116 billion spent on programs for the poor.

Where's all that money go? There's direct subsidies to agribusiness ($18 billion a year), to export companies, to maritime shippers, and to various industries-- airlines, nuclear power companies, timber companies, mining companies, automakers, drug companies. There's billions of dollars in military waste and fraud. And there's untold billions in tax credits, deductions, and loopholes. Accelerated depreciation alone, for instance, is estimated to cost the Treasury $37 billion a year-- billions more than the mortgage interest deduction. (Which itself benefits the people with the biggest mortgages. But we should encourage home ownership, shouldn't we? Well, Canada has no interest deduction, but has about the same rate of home ownership.)

For more, see Mark Zepezauer and Arthur Naiman's informative little book, Take the Rich Off Welfare.

How about social spending? Well, putting aside the merely religious consideration that the richest nation on the planet can well afford to lob a few farthings at the hungry, I'd argue that it's social spending-- the New Deal-- that's kept this country capitalistic. Tempting as it is for the rich to take all the wealth of a country, it's really not wise to leave the poor with no stake in the system, and every reason to agitate for imposing a new system of their own. Think of social spending as insurance against violent revolution-- and again, like any insurance, it's of most benefit to those with the biggest boodle. (See also my page on whether welfare does any good).

Who gets to sit on the tax?

Come election season, Steve Forbes, among other millionaires, will be pushing plans for a flat tax. These proposals need to be absorbed with a carload of salt.

A plan where everyone's taxes are lowered is of course simply a tax cut. Here, once again, the question to ask as a voter and citizen is, what government services do you want to cut? Somehow I don't think Steve is proposing to slash corporate welfare or defense. It's more likely a way to attempt to cut social spending through the back door. People like to hear about tax cuts; they don't like to hear about service cuts, even though they're financially equivalent.

A revenue-neutral plan won't change total receipts any-- it'll just redistribute it. Here you have to ask, who gets shafted?

You can't exactly make the poor pay more taxes-- they don't have the money. That leaves only one way to flatten the tax rates-- that is, reduce the taxes the rich pay: soak the middle class. If tax rates go down on the rich, and we're not cutting total taxes, the middle classes have to pay more.

So Steve and the others want the government, already pretty much a subsidiary of the large corporations, to be subsidized even more by the rest of us. About all I can say is, if the American people are stupid enough to swallow this, they deserve to pay for it. (Fortunately, as we saw with Monicagate, the American people are not as stupid as their leaders.)

This is pretty shameless, but it's much of a piece with Republican practice in general. For years some nosy folks (such as Sen. Moynihan) have been investigating what states pay the most to the federal government, and which states get the most benefits back. What a surprise: the biggest winners are the western and southern states that vote Republican; the biggest losers are the northeastern states that vote Democratic. Those who whine the most about taxes are those who suck the most from the public trough.

They won't be happy, I suppose, until they can reconstitute a truly medieval system, in which the nobles pay no taxes at all.

The marriage tax

While we're at it, what about the marriage penalty? Why in heavens are we penalizing marriage?

We aren't. This is a good example of politicians' weasel-talk. There's no marriage penalty-- there's a double-income penalty.

For instance, suppose you make $50,000 of taxable income (after deductions and exemptions) and your spouse doesn't work. Together you pay $8500 in taxes. A single person with the same income pays $10,700. You're enjoying a $2200 marriage bonus. (Even more, if you've taken the standard deduction.)

The penalty comes for double-income marriages. E.g. you make $50,000, and your spouse makes $40,000. You pay $19,700 in taxes; if you were both single you'd pay a total of $18,600-- about $1100 less.

Is it fair to tax double-income households more? Well, why not? If you have a double income, you can certainly afford to pay more than those of us who have just one.

And again, reducing this "penalty" for double-income households means increasing taxes on single-income households.

Exercises for the Republican reader:

Write a rebuttal justifying the corporate subsidy of your choice, respecting the conservative principle that the tax system cannot be used for social engineering.

Write a homily, suitable for use in Sunday school, explaining why Jesus should have condemned the sheep who demeaned the poor by feeding and clothing them, and blessed the rich man for living in splendor while Lazarus suffered.

Take your favorite flat tax proposal and your last 1040, and have your acountant calculate how much money it will save you. Find the names of the five or six middle-class people who will have to make up that shortfall, and write them a nice thank-you note.

Compare the GNP with the rate of taxation over the last fifty years-- e.g. the boom years of the '50s with their 90% marginal tax rate-- and practice explaining that high tax rates discourage investment until you can do it with a straight face.

http://www.zompist.com/richtax.htm

Most people believe that paying their taxes diligently and timely will help them to get a good night's sleep and so, they discharge their tax liability year after year by paying income tax on time. However, many taxpayers remain ignorant about paying another form of tax - which is charged on the assets gathered by them. Known as the Wealth Tax, it is the less famous brother of income tax, which is payable on the wealth accumulated by individuals over the years. As it is an additional tax, it is levied over and above income tax.

While income tax is payable on the total taxable income earned by an individual in one year, wealth tax is paid on the possession of certain properties which fall under the Wealth Tax Act of the Indian taxation system. Here are some facts about wealth tax that all taxpayers should know....

What is Wealth Tax?

Wealth tax is a direct tax levied on the ownership of certain assets by individuals and Hindu Undivided Families (HUFs) even though these assets may not generate any income. It is an annual tax and is imposed with reference to the previous financial year or the present assessment year. It is governed by the Wealth Tax Act, 1957.

Which assets attract wealth tax?

The assets which are taxable under the Wealth Tax Act are residential property other than one house, guesthouse, farmhouse; motor cars; precious metals including those in the form of jewellery, gold, furniture, utensils or other articles; aircrafts, yachts, boats; urban land and cash in hand in excess of Rs. 50,000.

In addition to these, all assets transferred by individuals to their minor children and to a spouse for inadequate consideration also attract wealth tax.

Which assets are exempt from wealth tax?

Assets such as financial instruments, a residential house, cars, property, stock-in-trade or other assets which are used commercially (for business purposes) do not attract wealth tax. Plus, wealth tax is not imposed on those residential properties which are rented for at least 300 days in a year.

Residential status also effects total taxable wealth

In India, the extent of taxable wealth for individuals differs with their residential status. For resident Indians, net taxable wealth will include all assets in India and abroad whereas for non-resident Indians, net taxable wealth includes only those assets which are in India.

How to calculate wealth tax?

Wealth tax is paid when an individual's net taxable wealth minus his/her total outstanding debt on all such assets (that are eligible for wealth tax) is more than Rs. 30 lakh, as on valuation date (31st March of a financial year). It is levied at 1% of the net taxable wealth exceeding Rs. 30 lakh.

When and how to pay wealth tax?

Taxpayers can pay wealth tax by using the Challan ITNS 282, before filling for wealth tax returns.

There is heavy penalty for late/non-payment

Late payment of wealth tax attracts a penalty of 1 % interest per month for each month of delay. Moreover, in cases of non-payment of wealth tax/tax evasion, the tax officer can start tax recovery proceedings in which a heavy penalty of as much as five times the amount of tax due can be slapped on the defaulter. Plus, in extreme cases the defaulter may also be sentenced to jail term.

http://www.rupeetimes.com/article/fixed_deposits/some_quick_facts_about_wealth_tax_in_india_7846.html

CII president Adi Godjrej is believed to have "strongly advised" Chidambaram that any move to raise taxes on the rich would prove counter-productive at a time when the compelling need is to revive the economy through higher corporate investments. The Economic Times today quotes Surjit Bhalla as saying that none of the economists who have attended pre budget meetings have supported a raise in marginal taxes. The paper also makes the point that over time a 'hostile tax regime' could change the direction of flows into India.

Venky Vembu has written yesterday in his piece, History lesson: Mr FM, when it comes to taxes, less is more:

India's own experience of taxation proposal over the decades points to the folly of having peak tax rates at very high levels. In Indira Gandhi's time, for instance, the peak tax rate was 97.5 percent, which meant that beyond a certain income threshold, the government took away every rupee of your earnings. Such a high tax rate provides very little incentive for people to disclose their earnings – or even to be industrious and work hard and earn well – since they never got to enjoy the fruits of their labour.

On the other hand, India's experience of lowering peak tax rates progressively in the two decades since the economic reforms of 1991 has validated the wisdom of the Laffer Curve model, which established the relationship between possible rates of taxation and the resulting levels of government revenue.

http://www.firstpost.com/business/raising-taxes-will-india-lose-its-rich-to-singapore-and-dubai-592967.html

Wed, Jan 23, 2013 at 09:40

Santosh Nair

Moneycontrol.com

Finance minister P Chidambaram on Tuesday assured a gathering of global investors in Hong Kong that the government will not raise taxes in the upcoming Budget and that the fiscal deficit target would be met amid a stable tax regime.

Here is an extract from a note by investment bank Citi, which hosted the conference:

"…the FM was decidedly more positive. He suggests the fiscal deficit target will be met, taxes will not be raised the tax regime will be stable, and while policy will and should be biased towards the poor, the Budget will offer a lot."

It is not clear from the note if the Finance Minister has only foreign institutional investors in mind when he says that taxes will not be raised. By deferring GAAR and diluting some of its key provisions, the Finance Ministry has already signaled that it will do everything possible to keep foreign investors in good humour. At the same time, media reports over the last couple of weeks suggest that the government is considering ways to raise more taxes. The government may not have too many options other than increase taxes, considering that it has not shown much resolve to trim subsidies. And with general elections coming up in about 15 months, the government may not have much leeway on that front, given political implications.

FIIs have net pumped in net USD 2.67 billion into Indian equities in January so far, the highest ever in a single month. India badly needs foreign fund flows at this point, given its widening current account deficit, and to that extent, the government's pampering of FIIs is understandable.

But it is also important that the government figure some way to channelize domestic liquidity into the capital markets. The rally since October has been driven largely by foreign money. And stock market traders will tell you that declining trading volumes clearly points to lack of domestic participation in the rally.

According to an article in Business Standard, average daily volumes in the cash, futures, and options markets so far in 2012-13 are down 7, 13 and 20 percent respectively, compared to the previous year. This is despite benchmark indices being at a two-year high.

As much as the Finance Minister is eager to woo foreign investors, he also needs to sit with domestic money managers and figure out a way by which domestic savings can be attracted to stocks and bonds. As economists and financial market experts have been repeatedly saying, short term measures, like hiking import duty on gold for one, do not address the core issue of why domestic liquidity is flowing into unproductive assets like gold and land.

http://www.moneycontrol.com/news/market-edge/budget-2013-14-chidambaram-rolls-red-carpet-for-fiisabout-locals_811861.html

23 JAN, 2013, 07.00AM IST, RAM SAHGAL,ET BUREAU

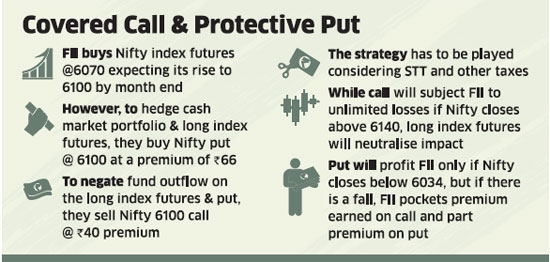

Foreign investors profess their love for Indian market again by adopting an innovative put-call strategy

They initiated the strategy when Nifty futures traded around 6050-6070, hoping the index would rise to 6100 or slightly above that level till the RBI's policy declaration on January 29. The markets have priced in a 25-basis points cut, but analysts say indices could correct by 5-7% if the central bank does not cut rates.

The three-pronged strategy involves buying index futures first to profit from a rise in markets and to maximise their cash holdings. On the second leg, FIIs purchase index put options giving them a right to sell the Nifty index if the market falls below a certain level called the strike price. On the last leg, they sell index call options to negate the outflows from the purchase of index futures and index put options.

The strategy is complex, but can be simplified. Based on last Friday's levels, an FII, which owns shares comprising Nifty 50, purchases Nifty index futures around Friday's closing levels of 6070 for Rs6,070 as it feels the index could rise to 6100 following a postponement of anti-tax avoidance rules and partial decontrol of diesel prices, which would increase foreign inflows and narrow the fiscal deficit.

However, to protect itself from an unexpected fall, theFII also buys a Nifty put option of 6100 by paying a premium of Rs66 to ensure that if the index falls from the current levels, the gain on the put will partly offset the loss on long index futures.

The expense of Rs6,136 (6070 on the futures plus 66 on the call) is partly negated by the FII selling a call option of 6100 strike - the price at which Nifty can be purchased even if the index exceeds that level - for Rs40. Thus, the FII's outflow is reduced to Rs6,096 (6136-40 premium received).

If the Nifty rises to 6100 by January end or earlier, the FII's profit, excluding STT and other taxes, will be Rs4 (40 premium on call plus 30 rise of index futures minus 66 loss of premium on put), apart from an notional gain of Rs30 on its cash market holdings of Nifty shares. This is because the rise in the Nifty will be reflected in Nifty constituents.

However, instead of rising by 30 points to 6100, if the Nifty falls by 30 points from Friday's level of 6070 to 6040, the FII will still be left with a profit, ex-taxes, of Rs4 --(40 plus 30 which was received on put position) minus 66 (fall in index futures and part loss on put).

There will, of course, be an unrealised loss of Rs30 on their cash portfolios, but FIIs have initiated this strategy because they are bullish, say derivatives analysts.

http://economictimes.indiatimes.com/markets/stocks/market-news/foreign-investors-profess-their-love-for-indian-market-again-by-adopting-an-innovative-put-call-strategy/articleshow/18142179.cms

Troubled Galaxy Destroyed Dreams, Chapter: 836

Palash Biswas

Mobile: 919903717833

Skype ID: palash.biswas44

What does tax reform mean in India? More stimulus , more concession for the rich as well as super rich as they never belong to the excluded communities selected for systematic ethnic cleansing! Pre budget debate as well as policy making is focused on one point agenda that the rich in India should not be taxed as it would stall tax reforms. We have witnessed the GAAR episode. We have been witnessing continuous balance of payment crisis just because of bygone tax in lacs and sustained fiscal deficit due to foreign debt to balance the payment. Finance Minister P Chidambaram is proving himself industry friend unprecedented at the cost of the mango people in the banana republic.Asserting that India continues to be a "very good" investment destination, Urban Development Minister Kamal Nath today said the government would roll out more policy reforms in the next couple of months.Nath also said stress and distress are in Western economies, not in India. He is leading the Indian delegation at the World Economic Forum ( WEF) annual meet.

India has a well developed tax structure. The power to levy taxes and duties is distributed among the three tiers of Government, in accordance with the provisions of the Indian Constitution. The main taxes/duties that the Union Government is empowered to levy are:- Income Tax (except tax on agricultural income, which the State Governments can levy), Customs duties, Central Excise and Sales Tax and Service Tax. The principal taxes levied by the State Governments are:- Sales Tax (tax on intra-State sale of goods), Stamp Duty (duty on transfer of property), State Excise (duty on manufacture of alcohol), Land Revenue (levy on land used for agricultural/non-agricultural purposes), Duty on Entertainment and Tax on Professions & Callings. The Local Bodies are empowered to levy tax on properties (buildings, etc.), Octroi (tax on entry of goods for use/consumption within areas of the Local Bodies), Tax on Markets and Tax/User Charges for utilities like water supply, drainage, etc.

In the wake of economic reforms, the tax system in India has under gone a radical change, in line with the liberal policy. Some of the changes include:- rationalization of tax structure; progressive reduction in peak rates of customs duty ; reduction in corporate tax rate; customs duties to be aligned with ASEAN levels; introduction of value added tax ; widening of the tax base; tax laws have been simplified to ensure better compliance. Tax policy in India provides tax holidays in the form of concessions for various types of investments. These include incentives to priority sectors and to industries located in special area/ regions. Tax incentives are available also for those engaged in development of infrastructure.

Major global companies including Novartis, BAE Systems and Philips today expressed interest in expanding their businesses in India. Heads of the multi-national companies have shown keenness to shore up their operations in India during their meetings with Commerce and Industry Minister Anand Sharma, who is based in Davos now to participate in the annual WEF event.What does it mean? do you need any explaination? Just read the policy statements. Here you are!

"Watch the upcoming budget closely: it will prove that we mean business."

With those upbeat words – and a pledge to restore the Indian economy to a higher growth orbit next year – Finance Minister P Chidambaram, accompanied by a high-power Finance Ministry delegation, wooed investors in Hong Kong on Tuesday.The First Post reports.

At a closed-door session with investors – representing sovereign funds, wealth funds and asset management companies – Chidambaram hard-sold the India story, and sought to allay investors' concerns that the UPA government lacked the political will to do what it takes.

The Minister said he had been able to "bury the ghost" of GAAR. Reuters

Some of the investors who attended the investment roadshow that Chidambaram and his All-Star team got on the road ahead of Budget 2013 told Firstpost on condition of anonymity that the Minister was repeatedly asked about the government's ability to "stay the course" on unpopular but necessary reforms.

Investors also quizzed Chidambaram on the prospects of a sovereign rating downgrade if the government overshot its deficit targets. He, in turn, assured them that he would stick to his targets – no matter what.

"Under no circumstance will I agree to a breach of the fiscal deficit target of 5.3 percent of GDP," Chidambaram told mediapersons later.

The steps that the government had taken in recent weeks – such as the diesel price deregulation – had "assured everybody that there will not be a rating downgrade," he added. "They were concerned about our ability to stay the course after we announced the decisions. They are happy that we stayed the course after announcing FDI in multi-brand retail."

Investors' concerns that fuel price rationalisation – which was an important componenent of fiscal consolidation – would not be implemented had been sufficiently allayed, Chidambaram said. "Even the small steps we have taken have reassured them… Each of the measures has boosted their confidence in the Indian economy," he added.

Investors also pressed Chidambaram for clarity on the GAAR provisions, even though their implementation has been put off until 2016.The Minister said he had been able to "bury the ghost" of GAAR. "I explained to investors all the measures we have undertaken on GAAR, and pointed out that the stock market had received the proposals well. There is universal acknowledgement that we have handled the GAAR situation fairly effectively," he claimed.

The Indian economy, Chidambaram said, is "undeniably growing faster"; only China and Indonesia were growing at a faster pace. Yet, he noted, this wasn't sufficient, and there was a compelling need to accelerate growth."

The first step towards getting the growth engine revving was fiscal consolidation and showcasing a commitment to fiscal prudence. "We will achieve the targeted fiscal deficit of 5.3 percent of GDP this year, and for the next year, I will budget for a fiscal deficit of no more than 4.8 per cent next year."

GDP growth in 2013 would be between 6 and 7 percent, particularly since there had been a revival of investor confidence. "If investment gathers pace, we should get back to our growth rate of 8 per cent," Chidambaram said. "India's potential growth rate is above 8 per cent above. We have done it before. We will do it again."

Flashes of the petulance that Chidambaram has exhibited in recent times with the RBI, which has not heeded hints to lower interest rates, were again visible at the media briefing. Asked about the prospects for lower interest rates given that the RBI's focus on fighting inflation, Chidambaram said: "I don't manage the RBI. I merely convey the views of the government. It is for the RBI to take a call. Our stated position is that the RBI must balance between the need to stimulate growth and contain inflation."

"Policy reforms will continue and we will roll out more (reforms) in next couple of months," Kamal Nath, who is also in charge of Parliamentary Affairs, told PTI here.

In response to a query on whether the government would continue with policy measures for economic reforms on top of the recent decisions, he said" "Yes we are continuing."

Nath, who was instrumental in pushing the FDI reforms in the Parliament last month, stressed that the country is an attractive investment destination.

"India continues to be a very good investment destination and we have no stress or distress in our economy. The stress and distress lie in the western countries today. India is adapting to growth realities and the US and Europe are in distress," the Minister said.

In recent months, the government has unleashed a wave of reforms to bolster the sagging economic growth, which is expected to be around 5.7 per cent in the current financial year ending March 31, 2013.

The major reform measures include liberalisation of FDI norms in multi-brand retail and aviation sectors and partial de-regulation of diesel prices. Besides, steps have been initiated to keep subsidies under control.

India has buried the "ghost" of GAAR, Finance Minister P. Chidambaram said on Tuesday asserting that there is no threat of a rating downgrade in view of key economic decisions like allowing FDI in multi-brand retail and hiking fuel prices.Efforts to widen the tax base and increase revenues will continue, Finance Minister P Chidambaram said on Wednesday.He said there is revival of investor interest in India as a result of a number of measures taken by the government since September 2012.

The biggest threat to reforms in India is an unstable government at the Centre after 2014, finance minister P Chidambaram told investors and analysts in Singapore on Wednesday as he laid defined the broad contours of the economic agenda in the coming months.The Mint reports.

"The FM hopes to pass the Insurance Bill and the Pension Bill in the budget session of Parliament. He mentioned that behind the noise, there were quiet negotiations with the opposition parties and support from them," said a research note Bank of American Merrill Lynch that hosted a meeting between Chidambaram and investors in Singapore.

The Goods and Services Tax (GST) is unlikely to be passed by April 2013. "But the FM hopes to introduce the Bill in the monsoon session and pass it in the winter session in December this year," the report said.

Billed as India's biggest tax reform initiative, GST promises to stitch together a common national market by replacing a welter of local levies such as value-added tax (VAT) and octroi by a single tax.

"If there is a consensus with the states on these issues, the FM is hoping to move the GST legislation in the monsoon session of Parliament and pass the Bill in the winter session," the report said.

As reported in HT on January 22, Chidambaram promised a stable tax regime maintaining that efforts would be made to widen the tax base.

The finance minister was confident of keeping the fiscal deficit-broadly refers to the amount of money that the government borrows to fund its expenses — for this year at 5.3% of GDP.

Ahead of next week's monetary policy, Finance Minister P. Chidambaram, on Tuesday, said the Reserve Bank of India (RBI) must strike a balance between the needs of pushing growth and controlling inflation.

"I don't manage the RBI. I just convey the views of the government. It is for the RBI to take a call.

"Our stated position is that the RBI must balance between the needs of stimulating growth and containing inflation," he told PTI.

The RBI is slated to announce its third quarter review of monetary policy on January 29 amid demands by industry that it should lower interest rates to boost industrial output, which contracted by 0.1 per cent in November.

Before announcing the policy, the RBI Governor holds a customary meeting with the Finance Minister.

In order to contain inflation, the RBI has refrained from lowering interest rates despite nudging by Finance and Commerce ministries that it should take steps to address concerns on growth.

Inflation based on wholesale prices declined to a three-year low of 7.18 per cent in December. However, retail inflation rose for the third successive month in December to 10.56 per cent.

Mind you,Consumers across the country are likely to be burdened with another round of hike in prices including electricity tariffs, CNG powered transport, households using piped gas as the Petroleum and Natural Gas Ministry has moved the Cabinet for nearly doubling the price of domestically sold gas to $8 to 8.5 per million British thermal unit from the present $4.2 mmbtu, a move that could put an additional financial burden of nearly Rs. 7000 to Rs. 8000 crore on the common man.The Hindu reports.

Oil Ministry has moved a Cabinet note for nearly doubling the price of natural gas produced by state-owned ONGCBSE -1.14 % and OIL to $ 8-8.5 per million British thermal unit in the current year itself and for Reliance IndustriesBSE 0.31 % from April 2014.

The Ministry in a draft Cabinet note proposed accepting in toto the Rangarajan Committee recommendation of pricing domestically produced natural gas at an average of international hub prices and cost of imported LNG instead of present mechanism of market discovery.

Sources said ministry wants the pricing formula proposed by the panel to apply to all forms of natural gas - conventional, shale and coal-bed methane (CBM). Also, the price determined shall be applicable to all consuming sectors uniformly.

It, they said, wanted the new pricing guidelines to apply from 2013 itself on all domestically produced gas barring cases where it is either governed by a definite formula prescribed in the Production Sharing Contract (PSC) or the government had previously fixed a tenure for the same.

This essentially meant that RILBSE 0.31 % would get the new price only from April 1, 2014 upon expiry of the fixed five-year term of current rate of $ 4.205 per million British thermal unit.

State-owned Oil and Natural GasBSE -1.14 % Corp (ONGC) and Oil India LtdBSE -4.91 % (OIL) can, however, get the new rates this year itself for gas they produce from fields given to them on nomination basis by the government. Gas from nominated fields, called APM gas, is currently priced at $ 4.2 per mmBtu.

The Rangarajan panel suggested rates may also not apply to BG Group-operated Panna/Mukta and Tapti fields in the western offshore as the current rates of $ 5.57-5.73 per mmBtu for the fuel produced from these are derived from a pre-defined formula detailed in the PSC.

However, CairnBSE -1.32 % India's eastern offshore Ravva gas, which is currently priced at $ 3.5-4.3 per mmBtu, may be revised as per the committee recommendations.

Sources said the ministry said the Rangarajan panel report needs to be accepted so that domestically produced natural gas prices are fixed in a fair manner and in a way that incentivises production.

The panel had suggested taking a weighted average of the US, Europe and Japanese gas hubs or market price and then averaging it with the net imported price of liquefied natural gas (LNG) to give sale price of domestically produced gas.

Taking last year's publicly available consumption numbers and the prevailing price of gas in the three markets, the formula suggested by the Rangarajan committee gives $ 8-8.5 per mmBtu as the price of domestic gas.

Citing the recommendations of the recently set up Rangarajan Committee, which had come out with a roadmap for gas pricing, the Petroleum Ministry has sought an immediate hike in the price of gas sold by state-run Oil and Natural Gas Corporation (ONGC) and Oil India Limited (OIL) from $4.2 mmbtu to $8-8.5 mmbtu. However, in case of Mukesh Ambani-owned Reliance Industries Limited (RIL), which has been pushing for nearly tripling the gas price to around $13 mmbtu, the price hike will take effect from April 2014, the deadline set by the Empowered Group of Ministers (EGoM) in 2009.

By moving to push for almost double the hike in gas prices, the Petroleum Ministry has gone with the Rangarajan Committee recommendations for pricing domestically produced natural gas at an average of international hub prices and cost of imported LNG instead of present mechanism of market discovery. This despite plea by the Association of Power Producers (APP) that the Japanese import price formula suggested by the Rangarajan Committee should be removed from the hub prices as Japan LNG prices have been historically been much higher than the global market and this would distort the gas pricing. The APP has also contended that this would put an additional burden of Rs. 7000 to Rs. 8000 crore on the consumers.

In fact, government sources said the Petroleum Ministry has pitched that the pricing formula proposed by the panel be applied to all forms of natural gas - conventional, shale and coal-bed methane (CBM). Also, the price determined shall be applicable to all consuming sectors uniformly. The Ministry was keen on putting the recommendations into immediate effect and has strongly favoured that new prices should be applied without any further delay on all domestically produced gas barring cases where it is either governed by a definite formula prescribed in the Production Sharing Contract (PSC) or the government had previously fixed a deadline for the same.

Such a move would make gas produced from the KG basin bock of RIL automatically disqualified from revision of prices as under the EGoM approved guidelines, KG basin gas prices would be revised only after April 2014. ONGC and OIL will be the biggest beneficiaries of this government largesse this year for gas they produce from fields given to them on nomination basis by the government. Gas from nominated fields, called APM gas, is currently priced at $4.2 per mmBtu. The Rangarajan panel also suggested that rates may also not apply to BG Group-operated Panna/Mukta and Tapti fields in the Western offshore as the current rates of $5.57-5.73 per mmBtu for the fuel produced from these are derived from a pre-defined formula detailed in the PSC. However, Cairn India's eastern offshore Ravva gas, which is currently priced at $3.5-4.3 per mmBtu, may stand revised as per the latest recommendations.

The Rangarajan panel had suggested taking a weighted average of the US, Europe and Japanese gas hubs or market price and then averaging it with the net imported price of liquefied natural gas (LNG) to give sale price of domestically produced gas. Taking last year's publicly available consumption numbers and the prevailing price of gas in the three markets, the formula suggested by the Rangarajan committee gives $8-8.5 per mmBtu as the price of domestic gas.

Mr. Chidambaram was also hopeful that fiscal deficit will be contained within the targeted 5.3 per cent of the GDP this fiscal and trimmed to 4.8 per cent in the next. Growth is likely to climb to 6-7 per cent from 5.7 per cent expected in the current year, he said.

"There is universal acknowledgement that we have handled the GAAR situation fairly effectively and buried the ghost that GAAR will be some kind of a monster," he told PTI in an interview.

Here on a day's visit for an investor conference, the Finance Minister said as expected investors raised issues relating to the controversial provision of GAAR that was introduced in the 2012-13 Budget by his predecessor.

The General Anti-Avoidance Rules (GAAR) gave unbridled powers to taxmen to check evasion of taxes by foreign investors that created huge apprehensions among investors.

Last week, Mr. Chidambaram announced that GAAR implementation has been postponed by two years to 2016.

"On specific questions on GAAR and I took some time in explaining all the measures we have made to GAAR and told them how market has received it very well here. There is universal acknowledgement that we have handled the GAAR situation fairly effectively and buried the ghost that GAAR will be some kind of a monster," he said.

Kicking off his campaign to woo investment, Mr. Chidambaram met over 200 top investors at the "India for Investment Conference" organised by the Citibank and BNP Paribas.

He made a strong case for their investment assuring that all their concerns were being addressed and that the government has taken all measures including to contain fiscal deficit.

"It is a very well attended meeting. Virtually everybody who is anybody in the financial sector was here including wealth funds, sovereign funds, banks asset management companies. It gave me an opportunity to explain the economic situation in India, the steps we are taking to put the economy on high growth path," he said.

Mr. Chidambaram, who will be in Singapore on Wednesday on a similar mission, said India continues to post growth even now.

"We are undeniably growing faster," he said pointing that out only China and Indonesia are ahead of India.

"But this growth is not sufficient for us. We need to accelerate it. So I told them steps we are taking to accelerate growth," he said.

He said the first step in that direction is fiscal consolidation and commitment to the path of fiscal prudence.

"At that at the end of this year, we will achieve the target of 5.3 percent of fiscal deficit and next year I will budget for fiscal deficit no more than 4.8 percent," he said.

He said he has also explained to the international investors the number of measures taken in this regard.

"I thought it was a fruitful conference. I could get a sense of the concerns of investors. Happily many of the concerns were addressed in the last three of four months," he said.

Nevertheless,India's Foreign Direct Investment (FDI) inflows declined to a nearly two-year low of USD 1.05 billion in November 2012, mainly due to global economic uncertainties.

In November 2011, the country had attracted FDI worth USD 2.53 billion.

For the April-November period 2012-13, the inflows have declined by about 31 per cent to USD 15.84 billion, from USD 22.83 billion in the year-ago period, a senior official in the Department of Industrial Policy and Promotion (DIPP) told PTI.

According to experts, the global economic situation is the main reason for decline in the inflows.

"The global economic slowdown and lack of political consensus on FDI related matters are the reasons for decline," said Krishan Malhotra, Head of Tax and expert on FDI with corporate law firm Amarchand & Mangaldas.

Sectors which received large FDI inflows during the eight months of the current fiscal include services (USD 3.63 billion), hotel and tourism (USD 3.13 billion), metallurgical (USD 1.26 billion), construction (USD 1.01 billion) and automobile (USD 760 million), the official added.

India received maximum FDI from Mauritius (USD 7.2 billion), Japan (USD 1.56 billion), Singapore (USD 1.5 billion) the Netherlands (USD 1.09 billion) and the UK (USD 615 million).

The previous low was recorded in January 2011 when the FDI inflows slipped to USD 1.04 billion.

The inflows had aggregated to USD 36.50 billion in 2011-12 against USD 19.42 billion in 2010-11 and USD 25.83 billion in 2009-10.

In Singapore,Wooing over 300 city-based investors on the second leg of his east Asia tour, he said India is poised to grow at over 8 per cent from fiscal 2015-16 onwards.

"...efforts to keep on increasing the tax base will continue ... so that the tax revenue to the proportion of the GDP will also remain robust," he was quoted as saying by Sanjiv Bhasin, General Manager and CEO of DBS Bank, India.

The government, Minister said, was taking steps to bring down the fiscal deficit to 3 per cent of the Gross Domestic Product (GDP) in the next three to four years.

Mr. Chidambaram had on Tuesday told investors in Hong Kong that he was committed to keeping fiscal deficit to 5.3 per cent of the GDP in the current fiscal and reduce it further to 4.8 per cent in 2013-14.

As regards growth, the Minister was reported to have told investors that "India has fumbled, but so has most other economies worldwide".

The growth, Mr. Chidambaram had earlier said, was not likely to be below 5.7 per cent in 2012-13 and would improve to about 6-7 per cent in the next fiscal. Indian economy grew by 6.5 per cent in 2012-13.

The Minister, according to investors attending the meeting, has said that the Indian government was making efforts to put economy back on track.

In his over two-hour long interaction with investors, Mr. Chidambaram spoke on host of issues including fiscal deficit, current account deficit, expenditure management and slowing economy.

Mr. Chidambaram assured the investors that savings from subsidies would help bring down fiscal deficit, said Bhasin.

Among other things, the Minister said that efforts were on to ensure that the savings rate, which was as high as 35-36 per cent of the GDP, is raised to the same level.

Mr. Chidambaram also highlighted India's success in many fields including the Aadhar platform, and the country becoming the world's largest rice exporter as well as substantial exporter of wheat.