Changes in Income Tax Act in Accordance with DTC Would Burn Industry as well as AAM AADMEE! Vodafone will have to pay over Rs 11,000 crore tax, once the amendment to change the Income Tax Act is approved by Parliament!

Indian Holocaust My Father`s Life and Time - Eight HUNDRED EIGHTEEN

Palash Biswas

http://indianholocaustmyfatherslifeandtime.blogspot.com/

http://basantipurtimes.blogspot.com/

Changes in Income Tax Act in Accordance with DTC Would Burn Industry as well as AAM AADMEE!Mind you,The most negative point in the Budget was that the market responded negatively to the government's proposal to amend the Income Tax Act retrospectively from 1962 in the wake of the Vodafone tax case verdict.

British telecom major Vodafone will have to pay over Rs 11,000 crore tax, once the amendment to change the Income Tax Act is approved by Parliament, a Finance Ministry official said today.On the other hand,Telecom major Vodafone on Wednesday said the government's move to retrospectively amend income tax laws does not augur well for investors but asserted that it has no plan to exit India.

On Friday, the government introduced a retrospective clarification to Income Tax Act, virtually amending the law to ensure that cross-border transactions such as the $11 billion Vodafone-Hutchison deal of 2007 become taxable. The Supreme Court had earlier ruled that the deal was not taxable in India.The retrospective amendment in Income Tax Act, as proposed in the Union Budget 2012-13, would dent confidence of foreign companies investing in India, a group of industrialists and experts opined on Saturday.

The changes in the I-T Act will also have a bearing on other overseas deals of similar kind. It will send wrong signals to the market and could discourage investors as they will be forced to rethink on our tax laws, which are becoming too complicated.

If they do amend the Act retrospectively, it would send a chill down the market. The government can haul up anyone if changes are brought in the Act. Consequently, any asset registered or incorporated outside India will be deemed to be situated in the country if the share or interest derives, directly or indirectly. The value of the interest earned will be judged according to the assets they have in India. These amendments will take effect from April 1, 1962, and will apply to assessment year 1962- 63 and subsequent assessment years.

The problem is with the retrospective nature of the amendment. The Vodafone issue is a little bit of shock for the market. When the issue came to light, markets reacted negatively to it.

The excise hike will pull up prices. But the government had already given stimulus to various non-performing sectors in 2008; it also needs to raise money. I think that is fine as the stimulus cannot be given for an indefinite period.

The fiscal deficit target is good. But given last year's slippage, the market will go through the numbers with fine comb to see if it can be achieved.

The service tax hike was probably not required at this point but I don't think it will create too much of headache. The government needs to raise revenue.

Confusion still prevails over the status of the Rs 2,500-crore deposit money that the Income Tax (I-T) Department has refunded Vodafone.reports Business line.

With the Supreme Court dismissing the Centre's claim in the Vodafone tax case, the Mumbai Income Tax Department late Tuesday night made a refund of Rs 2,568 crore to Vodafone.The department deducted a TDS of about Rs 50 crore from the final amount.

The cheque was collected by lawyers representing the company.

Over the last few days, Income Tax officials have been working out various permutations and combinations for calculating the interest and TDS component on the principle amount of Rs 2,500 crore.

On Tuesday evening, as soon as news arrived from New Delhi about the dismissal of the petition, officials swung into action and issued the cheque, sources said. On January 12, 2011, Vodafone had deposited the money with the department.

According to the Supreme Court Web site, the same Bench (comprising the Chief Justice Mr S.H. Kapadia, Mr Justice Swatanter Kumar and Mr Justice K S Radhakrishnan) — which delivered the landmark verdict in the Vodafone tax case and then on Tuesday dismissed the Centre's review petition challenging its order — is slated to hear on Friday an application by the I-T Department.

The application seeks a three-month extension of the refund deadline in the light of the proposed amendments in the Union Budget 2012-13 to tax Vodafone-Hutch type deals, according to sources in the Government's legal team.

"They (Vodafone) will have to automatically pay the tax after approval of the amendments to the Finance Bill by Parliament. We don't need to send fresh tax demand notice to them," a Finance Ministry official told PTI.

The government yesterday refunded Rs 2,500 crore along with 4% interest to Vodafone following dismissal of its review petition against January 20 order by the Supreme Court.

The government had raised a Rs 11,000 crore withholding tax demand on UK-based telecom firm for its USD 11 billion acquisition deal with Hutchison Essar in 2007.

With an aim to clarify the "intent" of the Income Tax 1961 on taxation of overseas deals involving domestic assets, Finance Minister Pranab Mukherjee in his 2012-13 Budget has proposed to amend the law with retrospective effect, to ensure that such deals are taxed.

"You can only tax on the basis of existing law. We have no right to tax them, current law will prevail so long law is not changed," Law Minister Salman Khurshid had said yesterday after a meeting of senior Cabinet Ministers following dismissal of review petition by the apex court.

According to the Finance Ministry official, "an important question is about equity in taxation. While ordinary tax payer pays its taxes honestly, those who have huge wealth do not pay taxes by taking recourse to tax avoidance through creation of multiple structures and routing their investments through low tax and no tax jurisdiction."

In the USD 11.2 billion deal in May 2007, Vodafone had acquired 67% stake in the Hutchison-Essar Ltd (HEL) from Hong Kong-based Hutchison Group through companies based in the Netherlands and Cayman Island.

"As a practising businessman in India, this will not augur well for foreign direct investment and the country at large," Vodafone India's non-executive Chairman Analjit Singh said in response to a query on the proposal to amend tax laws.

Earlier in the day, a Finance Ministry official told PTI: "They (Vodafone) will have to automatically pay the tax after approval of the amendments to the Finance Bill by Parliament. We don't need to send fresh tax demand notice to them."

In Budget 2012-13, Finance Minister Pranab Mukherjee has proposed amending the Income Tax Act retrospectively from 1962 to bring under net overseas deals involving domestic assets.

This would have a bearing on Vodafone which won the legal dispute in Supreme Court over Rs11,000-crore tax claim raised on its $11-billion deal with Hutchison Essar in 2007.

"The question is not changing the rules of the game so substantially, particularly (since) Vodafone is one of the largest foreign direct investors in India where FDI is about $15-16 billion," Singh told a private news channel.

His comments a day after the government refunded Rs2,500 crore along with interest to Vodafone following dismissal of its review petition by the Supreme Court.

On whether Vodafone would look at pulling out of India, he said the question is not even on the table. "Vodafone is an institution, Vodafone is there for opportunity. No nobody from Vodafone has ever directly or indirectly conveyed anything like that, the question here is fair play," he said.

The government's proposed amendment has invited wrath of many a corporate honcho. Incidentally, US-India Business Council President Ron Somers on Wednesday said: "Vodafone kind of cases sent a wrong signal to investors. It is a little regressive in nature. However, we believe this is one-off case and overall business environment will remain investor-friendly."

The government on Saturday said it has not come out with any Voluntary Disclosure of Income Scheme (VDIS) by proposing changes in the Income Tax Act, which experts believe are some sort of concessions to tap black money.

"There is no intention of the government to give any sop in form of voluntary disclosure... We are tightening provisions, we are not relaxing provisions," Finance Secretary R S Gujral said, when asked about reports that government has sought to bring in a VDIS through back door. Finance Minister Pranab Mukherjee, in his Budget speech, had proposed a series of measures to deter generation and use of unaccounted money, which included taxation of unexplained money, credits, investments and expenditures, at the highest rate of 30 per cent irrespective of the slab of income.

Tax experts, however, said the government is giving an option to erring tax payers to admit unaccounted money at early stage and pay 30 per cent tax. "The government is giving an option that if you admit at an early stage, then you do not have to go through all the proceedings. The government is trying to reduce the litigations by giving concessional way for bringing back money", said Ernst & Young Tax Partner Hitesh Sharma.

Another expert, who did not want to be named, said the government hopes confiscatory penalty would force people to disclose black money. "It thinks that this measures will give the IT department option to arm twist the offenders. It is a kind of 'carrot and stick policy' to discourage evasion," he said.

Gujral said currently if unaccounted money is found with a person in an I-T raid, the person usually says that he was about to declare it in next income tax return.

| Compute your Tax Liability |

|

http://law.incometaxindia.gov.in/DIT/Xtras/taxcalc.aspx

Income-Tax Act, 1961 as amended by Finance Act 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990

| Section Wise | Chapter Wise |

| Section No : | Search : |

| ||||||||||||||||||||||||||||||||||||||||||||

http://law.incometaxindia.gov.in/DIT/Income-tax-acts.aspx |

7 changes you can expect in your money life

We got rid of the clutter; here is a list of most important Budget announcements that will affect you

Deepti Bhaskaran, Devesh Chandra Srivastava, Lisa Pallavi Barbora, Kayezad E. Adajania & Bindisha Sarang

What the finance minister, Pranab Mukherjee, said in the Budget will definitely have an impact on your financial life. However, a lot of small things that remained unsaid will also leave a mark on your money and savings. We give you a list of seven such changes you can expect in your money life.1. Insurancebecomes more about protection

Insurance so far has been less about protection and more about investment and tax saving. Budget 2012 has taken cognizance of this fact and has proposed to increase the sum assured limit as a multiple of the premium in order to enjoy tax benefits.

Under section 80C of the Income-tax Act, premiums paid towards a life insurance policy qualify for a tax deduction up to Rs. 1 lakh. But if the amount of premium paid in a financial year for a policy is in excess of 20% of the sum assured, then tax deduction is allowed only on the premium amount up to 20% of the sum assured. As for the benefits, according to section 10 (10D), death benefit in an insurance policy is tax-free, but any other benefit, such as maturity proceeds, is tax-free only if the premium is up to 20% of the sum assured.

The Budget has proposed to reduce this 20% limit to 10%. So to get tax benefit under sections 80C and 10 (10D), you will have to buy a cover at least 10 times the annual premium. Currently, you need to buy only five times the annual premium to enjoy tax benefit.

If you are purchasing a term plan, this proposal may not affect you since the sum assured in a term plan is several multiples of the premium. But if you are buying an investment-cum-insurance policy such as unit-linked insurance plans (Ulip) or traditional plans, this proposal will be of importance.

In Ulips, if you are below 45 years of age, the minimum sum assured that you can take is 10 times the annual premium in a regular premium payment plan. So in this case, you shouldn't worry. But if you are above 45 years of age or are buying a single-premium policy, ensure you buy a cover which is at least 10 times the premium.

Most traditional policies are structured to give you tax benefit. However, there are some that do not conform to the tax rules. The proposal has not only increased the protection element but also ensures that insurers are not able to dress sum assured as maturity benefit so that the policies enjoy tax breaks. The Finance Bill has defined the sum assured to mean the minimum amount assured under the policy when the insured event takes place at any time during the term of the policy.

Mint Money in February noticed policies that defined sum assured as the maturity benefit. In such cases, the maturity benefit or the sum assured was five times the premium paid. The death benefit—or the amount that goes to the beneficiary upon death of the policyholder—in such cases were the return of premiums at a specified rate.

Finance Bill 2012 has done away with this discrepancy; now the sum assured will mean the death benefit only.

Further, in order to ensure a minimum death benefit, the bill has proposed that the sum assured that qualifies for tax benefits—in other words it is at least 10 times the premium paid—will be the minimum death benefit that will be paid in any policy year.

In other words, if you pay a premium of, say, Rs. 1 lakh, the sum assured will have to be Rs. 10 lakh throughout the tenor. This is in order to check those policies that give a high level of sum assured in year one and subsequently bring down the death benefit.

Says P. Nandagopal, managing director and CEO, India First Life Insurance Co. Ltd: "Tax savings should be more about the tenor of investment and not about the design. Reducing cover policies caters to people who accumulate enough assets over time and need very little insurance later in their life. By having a minimum sum assured of 10 times the premium paid at all times, such policies will be affected."

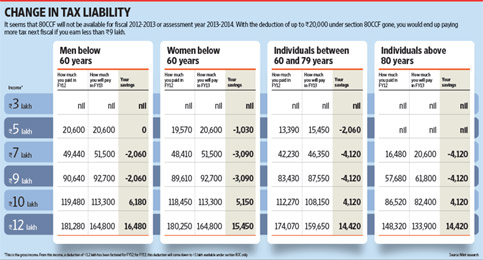

2. From tax-saving to tax-free bonds

In his Budget speech, the finance minister repeatedly focused on the need for infrastructure development and funding in that sector. It seems the ministry is now focusing on the tax-free bond route to channel small savings into this sector since the minister was silent on tax-saving infrastructure bonds. Tax-free bonds, which offer a tax-free interest at the end of the tenor but no deduction at the time of investment, are issued by government entities such as NHAI and HUDCO. This Budget has proposed to double the amount for these bonds to Rs. 60,000 crore.

In FY12, infrastructure finance companies, including IDFC Ltd, L&T Finance Ltd and IFCI Ltd, used tax-saving bonds to raise funds from small investors. Introduced in budget 2009-10, these were a good savings tool for small investors as they offered a tax deduction on the amount invested up to Rs.20,000 under section 80CCF. Along with Rs. 1 lakh deduction under 80C, this section bumped up your total deduction to Rs. 1.2 lakh.

The fact that any mention of this section was left out this time can result in investors not having this benefit for the coming financial year. It also means that infrastructure finance companies will not have this avenue as an attractive option to raise money from small investors. Whether this is going to be the case or not will be known through the course of the year as such a benefit can be introduced subsequent to the budget as well.

Sandeep Bhatnagar/Mint

Legal experts say leaving out 80CCF benefit is not a move in the right direction. Says Sanjiv Chaudhary, partner, KPMG, "There is a need to channel funds from savings of a larger base of investors into this sector. The investor demand for both types of bonds (tax-free and tax-saving) are separate and there is space for both." The infrastructure finance industry which was lobbying to increase the benefit under section 80CCF from Rs. 20,000 to Rs. 50,000 also isn't happy.

Impact on you: The removal of this section will impact you if you earn less than Rs. 9 lakh per annum. If you are below 60 years of age and your income is around Rs. 7-9 lakh, you will have to pay Rs. 2,060 more as income tax. For women below 60 years of age and in the same income bracket the loss is Rs.3,090. For senior citizens and very senior citizens, the loss is Rs. 4,120 for the same income bracket. The maximum savings in your overall income tax is Rs.16,480 for men below 60 years of age and with income of Rs. 11 lakh or above (see graph).

3. Service tax net tightens on insurance plans

Ulips: Last year the budget brought all the cost heads under the service tax net. So instead of being applicable only on mortality and fund management costs, service tax was made applicable on all the cost heads, including the policy allocation charge and policy administration charge. The service tax available on these charges was 10.3%, including cess. From the next fiscal this service will increase to 12.36%. Says G.V. Nageswara Rao, managing director and CEO, IDBI Federal Life Insurance Co Ltd: "This increase in service tax will mean an increase in premium. It is unlikely that insurers will absorb this increase in service tax."

Traditional plans: These plans, which do not disclose costs, the composite rate of service tax has been increased from 1.545% to 3.09% (including cess). This rate is applicable only in the first year; for subsequent years, the rate of service tax has been kept at 1.5%. So you will pay 50% extra service tax for the same sum assured in the first year.

Term plans: Here, a service tax of 12.36% will be applicable on the entire premium since term plans only charges you for the insurance cover.

Non-life plans: In the case of non-life plans such as health insurance or motor insurance, the service tax is levied on the entire premium.

4. MF distribution costs out of service tax ambit

Mutual fund (MF) distributors have reason to rejoice. They are now exempt from paying service tax from the commissions they earn from selling MFs. A day after it presented the Budget, the government of India issued a notification consisting a list of items that will now be exempt from the service tax. Till now, distributors used to pay a service tax of 10.3% (including 3% education cess) on the commission they received. Fund houses used to deduct this service tax on the distributor's behalf and pay it to the tax department.

At a time when distribution income appears to be on a decline on the back of regulatory restrictions as well as a drop in investor interest on account of lacklustre markets, distributors seem relieved by this measure as it will leave more money in their hands. "This is a great relief. It will result in a savings of at least Rs. 2,000 per month for most distributors. Even an ordinary distributor can save at least Rs. 1,000 every month by way of service tax exemption. If a distributor earns, say, Rs. 20,000, straightaway Rs. 2,060 used to get shaved off from his earnings. Now, he will get the entire Rs. 20,000," says K. Ramesh Bhat, president, IFA Galaxy, an all-India association of independent financial agents.

5. Savings account becomes tax friendly

The Union Budget has brought in a new section, 80TTA, which will enable you to keep small amounts of interest earned on your savings account out of the tax ambit.

According to the Budget proposal, you will get a deduction of up to Rs. 10,000 on interest earned from your savings accounts. Says Balwant Jain, charted accountant and CFO, Apnapaisa.com, "The finance minister proposes to grant a deduction in respect of interest on savings bank account to an individual and Hindu Undivided Family. The deduction is available in respect of interest on savings bank accounts earned by you from either a bank or a credit cooperative society or from a post office."

Impact on you: To earn Rs. 10,000 in interest, you would need to keep at least Rs. 2.5 lakh in your bank account (if it earns 4% per annum) and Rs. 1.66 lakh if you earn 6% per annum. Usually, people do not keep such lump sums in their savings account since other avenues such as bank fixed deposits fetch better returns.

Then there is a specific category that will benefit from this proposal: those with a taxable income below Rs. 5 lakh per annum. In the budget of 2011-12, salaried individuals earning income below Rs. 5 lakh were exempted from filing their returns; they were required to report the interest income from their bank accounts to their employers. Jain says, "A lot of salaried persons will be able to take the benefit of the scheme announced by the government where a salaried person is not required to file his income-tax return if his income is below Rs. 5 lakh and he has only income by way of interest on saving bank account not exceeding rupees Rs. 10,000."

6. Fillip to affordable housing

The Budget has extended the 1% interest subvention by another year for housing loans up to Rs. 15 lakh, where the cost of the house does not exceedRs. 25 lakh. The measure will ensure credit flow at relatively cheaper interest rate to buyers in the low-income group.

The Budget has also allowed external commercial borrowings (ECBs) for low-cost affordable housing projects and reduced withholding tax on interest payments on ECBs from 20% to 5% for three years. ECBs are instruments used in to access foreign money by Indian firms by way of loans and credits. "This should help developers mobilize financing in an otherwise difficult financing climate," says Gaurav Karnik, tax partner (real estate practice), Ernst & Young, an audit and consulting firm. While this strengthens the hands of those developers looking at affordable housing in tier II and III cities, homebuyers in this segment will also benefit. Says Nandita Tripathi, director (tax and regulatory services), KPMG, "Extending 1% interest subvention by a year aims to boost affordable housing in the country."

7. Check on unaccounted money

To contain use of unaccounted money in real estate's secondary market (where the properties being transacted in are not new), the government wants tax deduction at source (TDS). This may help smoother real estate deals and widen its scope.

The Budget has proposed to bring a new provision that every property buyer at the time of making payment by way of consideration for transfer of immovable property (other than agricultural land), will deduct a TDS of 1% of the agreed amount. Applicable from 1 October this would apply to transfers if the consideration exceeds Rs. 50 lakh for a property situated in an urban area and Rs. 20 lakh if the property is situated in another area. "A levy of TDS on immovable property transactions clearly intends to counter unaccounted money issues in the sector," says Tripathi.

At present, a TDS is applicable only when a non-resident Indian transfers immovable property.

Also See | Change in tax Liability (PDF)

deepti.bh@livemint.com

http://www.livemint.com/2012/03/19220956/7-changes-you-can-expect-in-yo.html

Union Budget 2012: Income Tax amendments and its implications

As part of his Union Budget 2012 proposals, the Finance Minister, Shri Pranab Mukherjee announced a number of amendments to the Income Tax Act. Let us try to understand a few of these amendments and its implications which impact the common man and / or the small scale business men:

Corporate Tax:

1. Minimum Alternative Tax (MAT) levied on partnership firms, Association of Persons (AOP) and Sole proprietory concerns claiming profit linked deduction, being tax holidays etc., under Chapter VIA: A GOOD MOVE TO BRING ALL ENTITIES AT PAR, THESE ENTITIES WOULD ALSO NOW BE REQUIRED TO PAY MAT @ 20.01% EVEN IN CASE OF NO TAXABLE PROFITS UNDER NORMAL COMPUTATION WHICH WAS HITHERTO APPLICABLE ONLY FOR CORPORATES.

2. Share capital / share premium credits in Private Companies to be taxed in the hands of the recipient unless the source of the funds of the investors are explained – A GOOD MOVE SINCE MANY CLOSELY HELD COMPANIES RESORT TO ONE TIME ENTRY TO ENHANCE THEIR EQUITY HOLDING IN THE BOOKS WHICH WILL NOW BE CURBED.

3. Share premium received in excess of the fair market value of the shares to be taxable as income in the hands of Private Companies: A GOOD MOVE AGAIN AIMED AT MITIGATING THE ONE TIME ENTRY MENACE, IT WILL ALSO CURB PROMOTERS BRINGING IN FUNDS WITHOUT ENHANCING THE AUTHORISED CAPITAL. THE ONUS WILL NOW BE ON THE RECEIPIENT TO PROVE THE FMV OF THEIR SHARES.

4. Undisclosed Income to be subject to tax at max. marginal rate of 30% and penalty of 10% to 90% to be levied – A RISKY MOVE, DURING SEARCH PROCEDURES, UNDISCLOSED INCOME IS SUBJECT TO TAX AT 30% EVEN IF IT FALLS BELOW THE BASIC EXEMPTION LIMIT. EARLIER, ONLY TAX AND INTEREST WAS LEVIED, NOW PENALTY AT 10%-90% ALSO TO BE LEVIED.

5. Exemption limit for compulsory tax audit for SMEs increased to INR 1 crore and INR 25 lakhs for professionals – A GOOD MOVE, RESULTING IN LESSER COMPLIANCE FOR SMALLER FIRMS AND PROFESSIONALS.

6. Time limit for claiming exemption u/s 80IA extended to 31.3.2012 for power sector – A GOOD MOVE, WILL CERTAINLY AUGMENT INVESTMENT IN POWER SECTOR

7. The weighted average deduction of 200% for in-house R&D extended by another 5 years – A GOOD MOVE, WILL AUGMENT AND ENCOURAGE COMPANIES TO SPEND ON INHOUSE R&D.

Personal Tax:

1. Basic threshold limit for chargeability of Income Tax increased from INR 1.80 lakhs to INR 2.00 Lakhs – A GOOD MOVE, WILL RESULT IN REDUCING THE TAX BURDEN BY INR 2,060/- FOR GENERAL TAX PAYERS. LESSER BENEFIT FOR WOMEN ASSESSEES SINCE THEY BENEFIT BY WAY OF ENHANCEMENT OF THE LIMIT BY ONLY INR 10,000/- AND CONSEQUENT TAX SAVING OF INR 1030/-, THE HIGHER EXEMPTION LIMIT FOR WOMEN ASSESSEES SINCE LAST MANY YEARS HAS NOW BEEN DONE AWAY WITH.

2. The higher ceiling in the tax slab for the 20% tax has been increased from INR 8.00 lakhs to INR 10.00 Lakhs – A GOOD MOVE, THIS WILL RESULT IN REDUCING THE TAX LIABILITY FOR PEOPLE HAVING INCOME ABOVE RS.8 LACS WITH A MAXIMUM BENEFIT OF INR 20,060/- FOR ASSESSEES HAVING INCOME OF INR 10 LAKHS AND ABOVE.

3. Additional deduction of upto INR 5,000/- provided for preventive medical checkup in the total ambit of INR 15000/- deduction u/s 80D – A GOOD MOVE, THIS WILL CERTAINLY ENCOURAGE PEOPLE TO GO FOR ANNUAL MEDICAL CHECKUP AND CLAIM DEDUCTION FOR THESE EXPENSES.

http://keralaitnews.com/features/finance/4586-union-budget-2012-income-tax-amendments-and-its-implications

Direct Taxes Code

From Wikipedia, the free encyclopediaThe Direct Taxes Code (DTC) is said to replace the existing Indian Income Tax Act, 1961.[1][2][3]

Contents |

[edit]Highlights of the Direct Taxes Code bill[4]

- Common threshold Income Tax exemption limit for men and women proposed at Rs. 2 lakh per annum (proposed), up from Rs. 1.8 lakh

- 10 per cent tax on annual income between Rs. 2-5 lakh, 20 per cent on between Rs. 5-10 lakh, 30 per cent for above Rs. 10 lakh

- Tax burden at highest level will come down by Rs. 41,040 annually

- Proposal to raise tax exemption for senior citizens to Rs. 2.5 lakh from Rs. 2.4 lakh currently.(NOTE:- Union budget 2011-12 already has proposed it.)

- Corporate Tax to remain at 30 per cent but without surcharge and cess.

- MAT to be 20 per cent of book profit, up from 18.5 per cent.

- Proposal to levy dividend distribution tax at 15 per cent.

- Exemption for investment in approved funds and insurance schemes proposed at Rs. 1.5 lakh annually, against Rs. 1.2 lakh currently

- Proposed bill has 319 sections and 22 schedules against 298 sections and 14 schedules in existing IT Act.

- Once enacted, DTC will replace archaic Income Tax Act.

- However, many provisions in Income Tax Act will be a part of DTC as well.

- FBT will be charged to the employee rather than the employer.

[edit]Salient features

- DTC removes most of the categories of exempted income. Equity Mutual Funds (ELSS), Term deposits, NSC (National Savings certificates), Unit Linked Insurance Plans (ULIPs), Long term infrastructures bonds, house loan principal repayment, stamp duty and registration fees on purchase of house property will lose tax benefits.

- Only half of Short-term capital gains will be taxed

- Surcharge and education cess are abolished.

- For incomes arising of House Property: Deductions for Rent and Maintenance would be reduced from 30% to 20% of the Gross Rent. Also all interest paid on house loan for a rented house is deductible from rent.

- Tax exemption on Education loan to continue.

- Tax exemption on LTA (leave travel allowance) is abolished.

- Taxation of Capital gains from property sale : For sale within one year, gain is to be added to taxable salary .

- Tax on dividends: Dividends will attract 5% tax.

- Medical reimbursement : Max limit for medical reimbursements has been increased to rupees 50,000 per year from current rupees 15,000 limit.

[edit]See also

[edit]Reference list

- ^ Direct Tax Code | DTC India 2009 | Deciphering DTC - Ernst & Young - India

- ^ Business Line : Features / Mentor

- ^ DTC's impact on India Inc

- ^ Direct tax code highlights

NCOME TAX RATES (AY 2012-13) - AMD & CO

- https://sites.google.com/site/.../income-tax/income-tax-rates-ay-2012-...

- The new and revised income tax slabs and rates applicable for the financial year (FY) 2011-12 and assessment year (AY) 2012-13 are mentioned below: ...

Tax code only from 2012

- www.business-standard.com › Home › Economy & Policy

- 31 Aug 2010 – NGOs unhappy with new foreign contribution law ... as the new legislation to replace the Income-Tax Act, 1961, is slated to come into force only ... the Centre expects to garner Rs 5,80417 crores in 2012-13 when DTC kicks in.

India's New Tax Structure for the Year 2012-13 | India Briefing News

- www.india-briefing.com/.../indias-tax-structure-year-201213-5297.ht...

- 1 day ago – Moreover, in the case of every company having total income taxable under section 115JB of the Income Tax Act (1961) and where such income ...

- [PDF]

2012 No. 00 (C. 00) CHARITIES INCOME TAX CAPITAL GAINS TAX ...

- www.hmrc.gov.uk/drafts/commencement-order-2012.pdf

- File Format: PDF/Adobe Acrobat - Quick View

- 3) for the meaning of the expressions "tax year" and "the tax year. 2012-13" for the purposes of the Income Tax Acts. Schedule 1 to the Interpretation Act 1978 (c.

COST INFLATION INDEX 2011-12 FINANCIAL ... - SIMPLE TAX INDIA

- www.simpletaxindia.net/.../cost-inflation-index-2011-12-financial.ht...

- 142/5/2011-TPL], DATED 23-6-2011. In exercise of the powers conferred by clause (v) of the Explanation to section 48 of the Income-tax Act, 1961 (43 of 1961), ...

Cost Inflation Index meaning and Index from financial ... - Tax Guru

- taxguru.in/income-tax/cost-inflation-index-meaning-and-in...

*

- by Sandeep Kanoi

- 6 Mar 2012 – Section 48 of the Income-Tax Act defin. ... Year 2011-12 · Cost Inflation Index for Financial Year 2011-12 / Assessment year 2012-13 ...

Proposed income tax amendments in Budget 2012-13-Part-2 ...

- www.caclubindia.com › Articles › Union Budget 2012

- 1 day ago – Proposed income tax amendments in Budget 2012-13-Part-2 ..... to in the said section applies, the provisions of the Income-tax Act shall apply ...

The Tax Corner

- www.thetaxinfo.com/

- SECTION 139 OF THE INCOME-TAX ACT, 1961 – RETURN OF INCOME ... OF INCOME UNDER SECTION 139(1) FOR ASSESSMENT YEAR 2012-13 ...

- [PDF]

Applied Direct Taxation - ICWAI

- www.myicwai.com/StudyMaterial/AppDirTax6.pdf

- File Format: PDF/Adobe Acrobat

- THE SOURCE OF INCOME TAX LAW. This Study Note includes. • Basic Concepts. • Rates of Income Tax for A.Y. 2012-13. • Definition. • Heads of Income ...

Important Information, Advance Income Tax For Corporate Assessee ...

- www.cahub.in/.../advance_income_tax_for_corporate_assessee_for_...

- corporate assessee for A.Y. 2012-13 is due for payment on or. before 15.03.2012. Assessee liable to pay tax u/s 211(1)(a) and (b). of the income tax act are …

Income Tax Act, 1961

| CONTENTS | |

| Income Tax India - FAQ - How to file Income Tax Returns, Income Tax Rates Applicable 2006-2007, 2007 - 2008, Important Dates... More | |

| Sections | Particulars |

| | |

| | |

| | |

| 1 | |

| 2 | |

| 3 | |

| 4 | |

| 5 | |

| 5A | |

| 6 | |

| 7 | |

| 8 | |

| 9 | |

| 10 | |

| 10A | |

| 10B | |

| 10C | |

| 11 | |

| 12 | |

| 12A | |

| 12AA | |

| 13 | |

| 13A | |

| 14 | |

| 15 | |

| 16 | |

| 17 | |

| 18 | |

| 19 | |

| 20 | |

| 21 | |

| 22 | |

| 23 | |

| 24 | |

| 25 | |

| 25A | |

| 26 | |

| 27 | |

| 28 | |

| 29 | |

| 30 | |

| 31 | |

| 32 | |

| 32A | |

| 32AB | |

| 33 | |

| 33A | |

| 33AB | |

| 33ABA | |

| 33AC | |

| 33B | |

| 34 | |

| 34A | |

| 35 | |

| 35A | |

| 35AB | |

| 35ABB | |

| 35AC | |

| 35B | |

| 35C | |

| 35CC | |

| 35CCA | |

| 35CCB | |

| 35D | |

| 35DD | |

| 35E | |

| 36 | |

| 37 | |

| 38 | |

| 39 | |

| 40 | |

| 40A | |

| 41 | |

| 42 | |

| 43 | |

| 43A | |

| 43B | |

| 43C | |

| 43D | |

| 44 | |

| 44A | |

| 44AA | |

| 44AB | |

| 44AC | |

| 44AD | |

| 44AE | |

| 44AF | |

| 44B | |

| 44BB | |

| 44BBA | |

| 44BBB | |

| 44C | |

| 44D | |

| 45 | |

| 46 | |

| 46A | |

| 47 | |

| 47A | |

| 48 | |

| 49 | |

| 50 | |

| 50A | |

| 50B | |

| 51 | |

| 52 | |

| 53 | |

| 54 | |

| 54A | |

| 54B | |

| 54C | |

| 54D | |

| 54E | |

| 54EA | |

| 54EB | |

| 54F | |

| 54G | |

| 54H | |

| 55 | |

| 55A | |

| 56 | |

| 57 | |

| 58 | |

| 59 | |

| 60 | |

| 61 | |

| 62 | |

| 63 | |

| 64 | |

| 65 | |

| 66 | |

| 67 | |

| 67A | |

| 68 | |

| 69 | |

| 69A | |

| 69B | |

| 69C | |

| 69D | |

| 70 | |

| 71 | |

| 71A | |

| 71B | |

| 72 | |

| 72A | |

| 73 | |

| 74 | |

| 74A | |

| 75 | |

| 78 | |

| 79 | |

| 80 | |

| 80A | |

| 80AA | |

| 80AB | |

| 80B | |

| 80C | |

| 80CC | |

| 80CCA | |

| 80CCB | |

| 80CCC | |

| 80D | |

| 80DD | |

| 80DDB | |

| 80E | |

| 80F | |

| 80FF | |

| 80G | |

| 80GG | |

| 80GGA | |

| 80H | |

| 80HH | |

| 80HHA | |

| 80HHB | |

| 80HHBA | |

| 80HHC | |

| 80HHD | |

| 80HHE | |

| 80HHF | |

| 80I | |

| 80IA | |

| 80IB | |

| 80J | |

| 80JJ | |

| 80JJA | |

| 80JJAA | |

| 80K | |

| 80L | |

| 80M | |

| 80MM | |

| 80N | |

| 80-O | |

| 80P | |

| 80Q | |

| 80QQ | |

| 80QQA | |

| 80R | |

| 80RR | |

| 80RRA | |

| 80S | |

| 80T | |

| 80TT | |

| 80U | |

| 80V | |

| 80VV | |

| 80VVA | |

| 81 | |

| 82 | |

| 83 | |

| 84 | |

| 85 | |

| 85A | |

| 85B | |

| 85C | |

| 86 | |

| 86A | |

| 87 | |

| 87A | |

| 88 | |

| 88A | |

| 88B | |

| 89 | |

| 89A | |

| 90 | |

| 91 | |

| 92 | |

| 93 | |

| 94 | |

| 95 | |

| 96 | |

| 97 | |

| 98 | |

| 99 | |

| 100 | |

| 101 | |

| 102 | |

| 103 | |

| 104 | |

| 105 | |

| 106 | |

| 107 | |

| 107A | |

| 108 | |

| 109 | |

| 110 |

http://www.vakilno1.com/bareacts/incometaxact/incometaxact.htm

Full coverage

Finance minister Pranab Mukherjee defends 'zero risk' BudgetIndia Today - Mar 17, 2012 He said he hiked service tax to 12 per cent because the objective is to reach GST. Finance minister Pranab Mukherjee, under fire from most quarters for presenting a "zero risk" Budget, said the government was committed to the passage of key reforms. India best international investor in Britain: PranabZee News - Mar 17, 2012 Ghaziabad: India has been the top international investor in Britain for three consecutive years, union Finance Minister Pranab Mukherjee said here Saturday. Talking to media persons, the finance minister said: "European nations have taught us ... In the game, but not a game-changerTimes of India - Mar 17, 2012 A few weeks ago, Pranab Mukherjee had complained that the prospect of unchecked fiscal deficits was giving him sleepless nights. Friday's Budget might ensure a few restful nights but is unlikely to cure him entirely of his insomnia . Service Tax on centuries? See, para 163, page 28 of Budget speechEconomic Times - Mar 17, 2012 On Friday, Pranab Mukherjee presented the budget, and Sachin Tendulkar scored his 100th 100. Then, they had a conversation. T: Have you put a service tax on scoring centuries? There's a rumour here... M: Absolutely not...I mean I don't think so...let ... Govt firm on early decontrol of diesel pricesIndian Express - Mar 17, 2012 Finance minister Pranab Mukherjee on Saturday indicated that the government is firm on early deregulation of diesel prices. In an interaction with financial newspapers, he also said if subsidy outgo threatens to exceed the projected levels in the ... Union Budget 2012: Petroleum sector reforms after Budget session, says Pranab ...Economic Times - Mar 17, 2012 The government indicated on Saturday that it will take up crucial petroleum sector reforms after the budget session of parliament is over. In a post-budget interaction with reporters, finance minister Pranab Mukherjee said the budget was not the right ... Will try for consensus on oil reforms after Budget session: FMBusiness Standard - Mar 17, 2012 As the prices of the Indian crude oil basket hover around $122-$125 a barrel, Finance Minister Pranab Mukherjee on Saturday said the UPA government would consult all political parties to build a consensus over petroleum reforms, once the Budget session ... Pranab hints at fuel price hike after Budget sessionHindu Business Line - Mar 17, 2012 Fuel prices may be hiked soon after the Budget session, the Finance Minister, Mr Pranab Mukherjee, indicated on Saturday. During a post-Budget interaction with financial newspapers, the Finance Minister said, "After the Budget session is over, ... Phone bills set to rise as service tax hike could be passed onZee News - Mar 17, 2012 New Delhi: With service tax set to rise from 10 to 12 percent, telecom companies on Saturday said tariffs for all telecom services will rise from the date the hike in tax is notified. "We are very disappointed with increase in service tax. Timing of implementation on GST, DTC remains uncertain: S&PNDTV - Mar 17, 2012 Apprehending "uncertainty" in implementation of key reforms like Goods and Services Tax and Direct Tax Codes by the government, global rating agencies have said the budgetary proposals fail to give a timeline on the same. "While the Finance Minister ... | RelatedTimeline of articles Number of sources covering this story

ImagesIBNLive.com  Wall Street Jou...  IBNLive.com  Aljazeera.com  BBC News  IBNLive.com  New York Times ...  IBNLive.com  Zee News Videos NDTV - Mar 17, 2012  * *IBNLive - Mar 16, 2012 *Mint - Mar 16, 2012  * *IBNLive - Mar 16, 2012  * *Mint - Mar 16, 2012 |

Income Tax Rates / Income Tax Slabs for Assessment Year 2012-13 (F Y 2011-12)

A. Individuals and HUFs

In case of individual (other than II, III and IV below) and HUF:-

| | Income Level / Slabs | Income Tax Rate |

| i. | Where the total income does not exceed Rs. 1,80,000/-. | NIL |

| ii. | Where the total income exceeds Rs. 1,80,000/- but does not exceed Rs. 5,00,000/-. | 10% of amount by which the total income exceeds Rs. 1,80,000/- |

| iii. | Where the total income exceeds Rs. 5,00,000/- but does not exceed Rs. 8,00,000/-. | Rs. 32,000/- + 20% of the amount by which the total income exceeds Rs. 5,00,000/-. |

| iv. | Where the total income exceeds Rs. 8,00,000/-. | Rs. 92,000/- + 30% of the amount by which the total income exceeds Rs. 8,00,000/-. |

Education Cess: 3% of the Income-tax.

II. In case of individual being a woman resident in India and below the age of 60 years at any time during the previous year:-

| | Income Level / Slabs | Income Tax Rate |

| i. | Where the total income does not exceed Rs. 1,90,000/-. | NIL |

| ii. | Where total income exceeds Rs. 1,90,000/- but does not exceed Rs. 5,00,000/-. | 10% of the amount by which the total income exceeds Rs. 1,90,000/-. |

| iii. | Where the total income exceeds Rs. 5,00,000/- but does not exceed Rs. 8,00,000/-. | Rs. 31,000- + 20% of the amount by which the total income exceeds Rs. 5,00,000/-. |

| iv. | Where the total income exceeds Rs. 8,00,000/- | Rs. 91,000/- + 30% of the amount by which the total income exceeds Rs. 8,00,000/-. |

Education Cess: 3% of the Income-tax.

III. In case of an individual resident who is of the age of 60 years or more but below the age of 80 years at any time during the previous year:-

| | Income Level / Slabs | Income Tax Rate |

| i. | Where the total income does not exceed Rs. 2,50,000/-. | NIL |

| ii. | Where the total income exceeds Rs. 2,50,000/- but does not exceed Rs. 5,00,000/- | 10% of the amount by which the total income exceeds Rs. 2,50,000/-. |

| iii. | Where the total income exceeds Rs. 5,00,000/- but does not exceed Rs. 8,00,000/- | Rs. 25,000/- + 20% of the amount by which the total income exceeds Rs. 5,00,000/-. |

| iv. | Where the total income exceeds Rs. 8,00,000/- | Rs. 85,000/- + 30% of the amount by which the total income exceeds Rs. 8,00,000/-. |

Education Cess: 3% of the Income-tax.

IV. In case of an individual resident who is of the age of 80 years or more at any time during the previous year:-

| | Income Level / Slabs | Income Tax Rate |

| i. | Where the total income does not exceed Rs. 5,00,000/-. | NIL |

| ii. | Where the total income exceeds Rs. 5,00,000/- but does not exceed Rs. 8,00,000/- | 20% of the amount by which the total income exceeds Rs. 5,00,000/-. |

| iv. | Where the total income exceeds Rs. 8,00,000/- | Rs. 60,000/- + 30% of the amount by which the total income exceeds Rs. 8,00,000/-. |

Education Cess: 3% of the Income-tax.

B. Association of Persons (AOP) and Body of Individuals (BOI)

i. Income-tax:

| | Income Level / Slabs | Income Tax Rate |

| i. | Where the total income does not exceed Rs. 1,80,000/-. | NIL |

| ii. | Where the total income exceeds Rs. 1,80,000/- but does not exceed Rs. 5,00,000/-. | 10% of amount by which the total income exceeds Rs. 1,80,000/- |

| iii. | Where the total income exceeds Rs. 5,00,000/- but does not exceed Rs. 8,00,000/-. | Rs. 32,000/- + 20% of the amount by which the total income exceeds Rs. 5,00,000/-. |

| iv. | Where the total income exceeds Rs. 8,00,000/-. | Rs. 92,000/- + 30% of the amount by which the total income exceeds Rs. 8,00,000/-. |

ii. Education Cess: 3% of the Income-tax.

C. Co-operative Society

i. Income-tax:

| | Income Level / Slabs | Income Tax Rate |

| i. | Where the total income does not exceed Rs. 10,000/-. | 10% of the income. |

| ii. | Where the total income exceeds Rs. 10,000/- but does not exceed Rs. 20,000/-. | Rs. 1,000/- + 20% of income in excess of Rs. 10,000/-. |

| iii. | Where the total income exceeds Rs. 20,000/- | Rs. 3.000/- + 30% of the amount by which the total income exceeds Rs. 20,000/-. |

ii. Surcharge: Nil

iii. Education Cess: 3% of the Income-tax.

D. Firm

i. Income-tax: 30% of total income.

ii. Surcharge: Nil

iii. Education Cess: 3% of the total of Income-tax and Surcharge.

E. Local Authority

i. Income-tax: 30% of total income.

ii. Surcharge: Nil

iii. Education Cess: 3% of Income-tax.

F. Domestic Company

i. Income-tax: 30% of total income.

ii. Surcharge: The amount of income tax as computed in accordance with above rates, and after being reduced by the amount of tax rebate shall be increased by a surcharge at the rate of 5% of such income tax, provided that the total income exceeds Rs. 1 crore.

iii. Education Cess: 3% of the total of Income-tax and Surcharge.

G. Company other than a Domestic Company

i. Income-tax:

- @ 50% of on so much of the total income as consist of (a) royalties received from Government or an Indian concern in pursuance of an agreement made by it with the Government or the Indian concern after the 31st day of March, 1961 but before the 1st day of April, 1976; or (b) fees for rendering technical services received from Government or an Indian concern in pursuance of an agreement made by it with the Government or the Indian concern after the 29th day of February, 1964 but before the 1st day of April, 1976, and where such agreement has, in either case, been approved by the Central Government.

- @ 40% of the balance

ii. Surcharge: The amount of income tax as computed in accordance with above rates, and after being reduced by the amount of tax rebate shall be increased by a surcharge at the rate of 2.5% of such income tax, provided that the total income exceeds Rs. 1 crore.

iii. Education Cess: 3% of the total of Income-tax and Surcharge.

Disclaimer:

All efforts are made to keep the content of this site correct and up-to-date. But, this site does not make any claim regarding the information provided on its pages as correct and up-to-date. The contents of this site cannot be treated or interpreted as a statement of law. In case, any loss or damage is caused to any person due to his/her treating or interpreting the contents of this site or any part thereof as correct, complete and up-to-date statement of law out of ignorance or otherwise, this site will not be liable in any manner whatsoever for such loss or damage.

http://finotax.com/itax/itaxrates.htm

No comments:

Post a Comment